Hongkong

Hongkong China

China

Hong Kong is an international financial center known for its stable economy and favorable conditions for international business. This system operates effectively because the city government closely monitors compliance with all legislative norms.

One of the most important elements of business management in Hong Kong is the audit of financial statements. This is a mandatory activity for all companies registered in this jurisdiction. Having an audit opinion allows businesses not only to meet legal requirements but also to demonstrate their reliability to investors, partners, and banks.

In this article, we will explore the key aspects of auditing in Hong Kong, starting with mandatory requirements and ending with practical recommendations for preparing financial statements for a successful audit.

Key Audit Requirements in Hong Kong

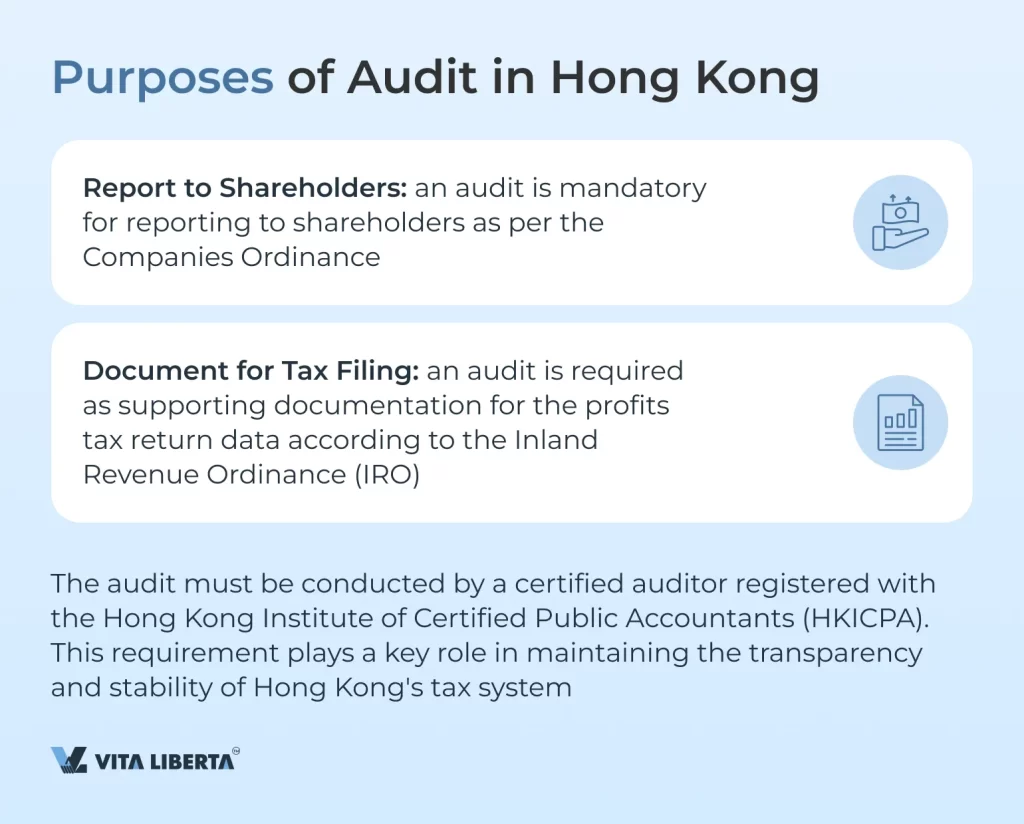

According to the Hong Kong Companies Ordinance (CO), an annual audit of financial statements is mandatory for all companies. In addition to this requirement, the Inland Revenue Ordinance (IRO) requires companies in Hong Kong to submit audited financial statements when filing a Profits Tax Return (PTR).

The main goal of the audit is to obtain an objective and accurate picture of the company’s financial condition, eliminating internal bias. This helps tax authorities and stakeholders, such as investors and partners, rely on the accuracy of the data.

Unlike other countries, in Hong Kong, an audit includes not only the verification of the company’s financial statements but also the verification of profits and taxes payable to the government.

If companies do not undergo an audit or intentionally misrepresent information, it can lead to a false representation of the business’s financial condition. Such practices make it impossible to properly comply with the requirements of the Hong Kong Inland Revenue Department (IRD), which can lead to serious consequences for the business.

Who is Exempt from Mandatory Audit in Hong Kong?

1. Dormant Companies

“Dormant” companies are those that have passed a resolution and submitted it to the Hong Kong Companies Registry to confirm this status.

It is important to understand that a “dormant” company is different from a company that is temporarily inactive. The status of a “dormant” company is formally established within the company and officially declared in the Companies Registry according to section 447 of the Hong Kong Companies Ordinance, Chapter 622. Only in this case can the company qualify for regulatory relief from mandatory audit requirements. An inactive company must comply with all legislative requirements without exceptions.

A dormant company must not conduct any significant transactions, except those permitted under section 447 of the Hong Kong Companies Ordinance, Chapter 622.

2. Foreign Companies Operating in Hong Kong

If a company is registered in a country where the laws do not require an audit of financial statements, and an audit was not conducted voluntarily, the IRD will accept unaudited financial statements as supporting documentation for the tax return.

If an audit was conducted, even if not required by the laws of that country, the audited financial statements must be submitted with the return.

3. Branches of Foreign Companies

If the head office of a company is located outside Hong Kong but has a branch in Hong Kong, the IRD usually accepts the unaudited financial statements of the branch. However, if necessary, a tax inspector may request a copy of the audited financial statements.

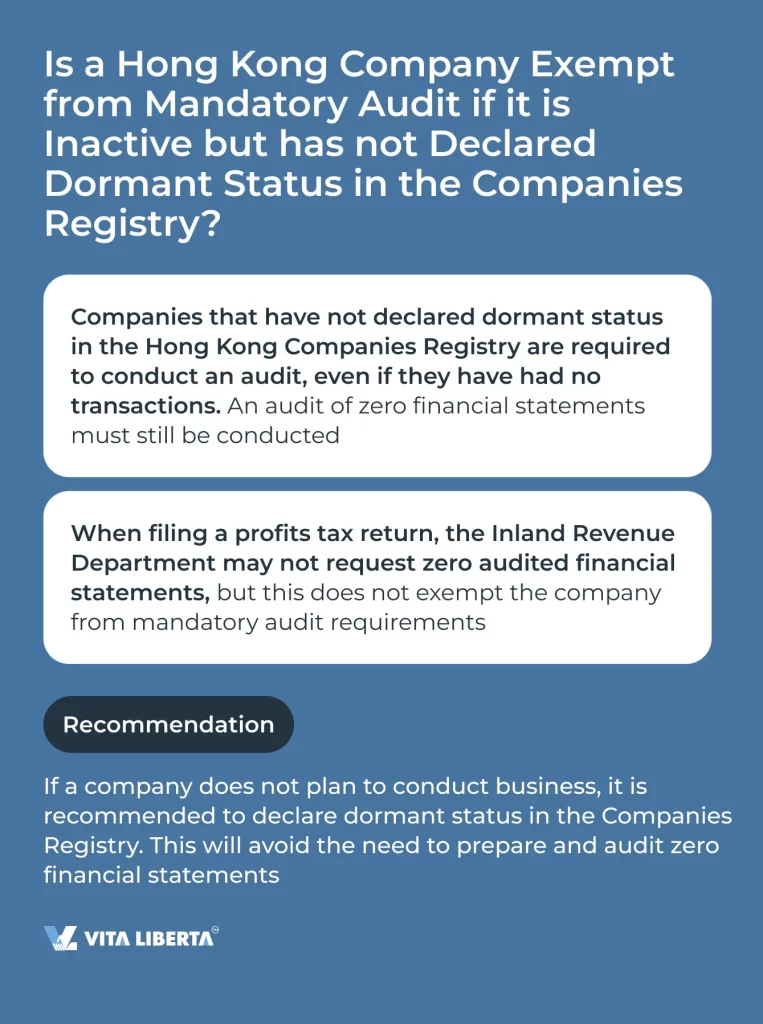

The absence of activity by a Hong Kong company, whose founders and management have not passed special resolutions and have not notified the Hong Kong Companies Registry of dormant status, is not a reason for exemption from mandatory audit of financial statements.

Practical Example

In the financial year 2022-2023, “XXX Limited” submitted a zero tax return. The company’s director signed a confirmation that no activity was conducted, and the tax authorities accepted the return without audited financial statements. This allowed the company to fulfill its obligations to the tax authority. Considering that the director and shareholder of the company are the same person, the issue of providing audited financial statements to investors did not arise.

However, in the next financial year (2023-2024), the company became active, necessitating the preparation of full financial statements and an audit. It was then discovered that audited financial statements were required for the first financial year in which the company had no activity.

Justification

The company did not declare dormant status, so an audit is legally required. The auditor must have access to all audit reports from previous years to form a correct opinion for the current period.

Therefore, an audit (even with zero values) must be conducted for the first financial year to ensure the audit for the second financial year is legally compliant. In this case, the auditor must adhere to audit standards and inform the company of any violations of the Companies Ordinance.

Appointment of an Auditor in Hong Kong

An auditor must be appointed for each financial year of the company.

Directors can appoint the first auditor before the first Annual General Meeting (AGM) of shareholders. Subsequently, the auditor can be reappointed at the AGM and will hold office until the end of the next AGM. If an auditor resigns, a new auditor must be appointed within one month.

Companies are required to hold an AGM at least once in a financial year and no later than nine months after its end.

If a company is not required to hold an AGM for the first financial year, directors can appoint an auditor before the start of the next financial year.

An auditor must be appointed for the financial year by a resolution passed at the AGM held for the previous financial year, except for companies not required to hold an AGM for the previous financial year.

If an AGM is not required, the auditor is appointed at a general meeting before the start of the next financial year. If an auditor is not appointed at the AGM, the company must do so at another general meeting.

Annual General Meeting (AGM) in Hong Kong

According to the Companies Ordinance, a company must hold an AGM for each financial year, not the calendar year. However, there are exceptions:

- Section 612(1): An AGM is not required if all matters are resolved by written resolution and documents are provided to members.

- Section 612(2)(a): A company with a single member is exempt from holding an AGM.

- Section 613: An AGM can be dispensed with by a written resolution of all members.

- Section 611: Dormant companies are exempt from holding an AGM.

Timing for Holding an AGM

- Private companies must hold an AGM within 9 months after the end of the reporting period.

- Other companies: An AGM must be held within 6 months after the end of the reporting period.

For the first reporting period, if it lasts more than 12 months:

- Private companies: 9 months after the first anniversary of incorporation or 3 months after the end of the reporting period, whichever is later.

- Other companies: 6 months after the first anniversary of incorporation or 3 months after the end of the reporting period, whichever is later.

The reporting period is the period in relation to which the company’s financial year is determined.

Objectives of the Audit and Appointment Dates of the Auditor in Hong Kong

| In accordance with the Companies Ordinance (CO) of Hong Kong | Under the Internal Revenue Regulations (IRO) | |

| Rationale | Annual Mandatory Audit | Mandatory Audit for PTR Submission |

| For whom it is intended | To the Management of the company at the annual general meeting of shareholders or other general meeting | To the Inland Revenue Department of Hong Kong |

| For what purposes is it provided? | To demonstrate the company’s financial results for the reporting period, confirmed by an independent party. | To confirm the reliability of financial statements by an independent party in order to confirm the correctness of the tax calculation. |

| Preparation and submission deadlines | Within 9 months after the end of the financial year. If the auditor is changed, a new one must be appointed within 1 month | Within 1 month of receiving the PTR. Subject to certain conditions and upon request, the deadline may be extended. |

| Who can be exempted | Dormant Companies | Dormant companies; Companies registered in countries that do not require mandatory audit of financial statements and that do not conduct it voluntarily; Branches of foreign companies in Hong Kong (may be requested by the tax inspector if necessary). |

Audit Standards in Hong Kong

Hong Kong Standards on Auditing (HKSA) are developed by the International Auditing and Assurance Standards Board (IAASB). These standards are based on International Standards on Auditing (ISA) and are adapted for the local context. The main goal is to regulate the audit process and ensure that companies’ financial statements meet international requirements. Compliance with these standards is mandatory for all auditors registered with the Hong Kong Institute of Certified Public Accountants (HKICPA), and any deviations may lead to disciplinary actions, including the loss of certification.

HKICPA is responsible for accrediting accountants and issuing certificates for professional practice, overseeing the professional conduct and standards of its members, establishing codes of ethics and accounting and auditing standards, and providing training and professional development.

Hong Kong Financial Reporting Standards (HKFRS) are also fully aligned with International Financial Reporting Standards (IFRS). Developed by HKICPA, these standards are intended for use in general-purpose financial reporting and other financial reporting by all commercial entities.

Audit Process in Hong Kong

The audit process consists of several stages, during which the auditor verifies and confirms not only the financial indicators but also the internal organization of the company. The goal of the audit is to ensure that the company’s financial statements provide accurate and reliable information about its condition. In Hong Kong, the audit process is similar to that in other countries and includes the following key steps:

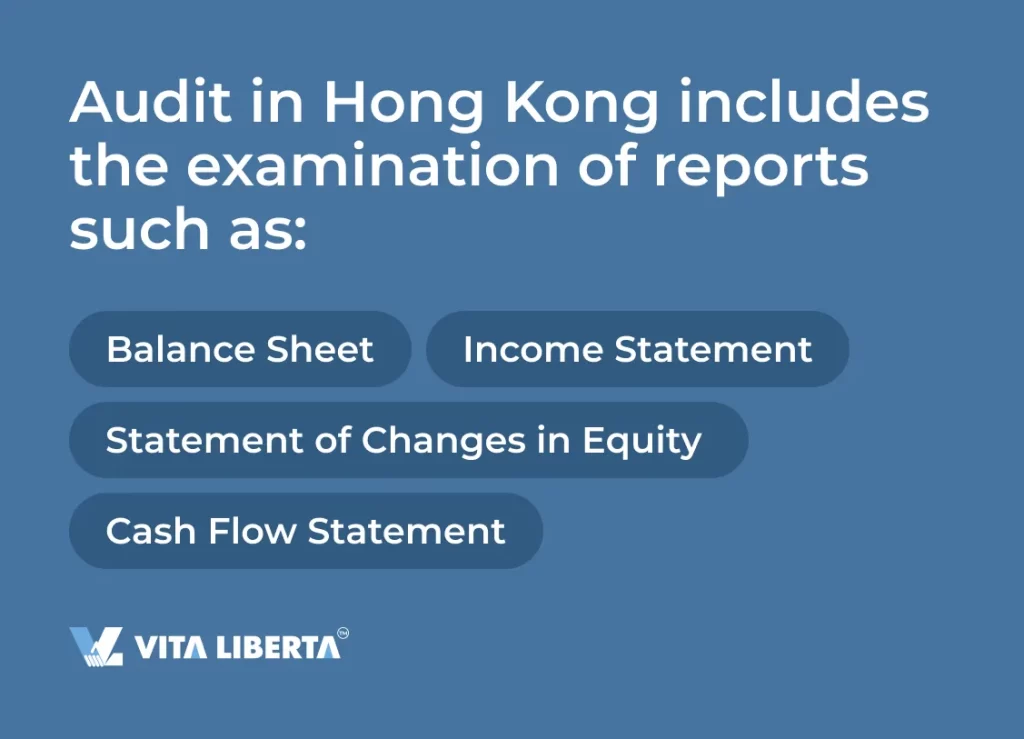

1. Preparation of Reports and Documents

The company’s management prepares financial statements, including the balance sheet, income statement, cash flow statement, and other necessary documents.

2. Verification and Analysis

Auditors begin the audit by examining the company’s activities, industry-specific factors, and other important aspects that may affect the audit. This helps to better understand what risks or uncertainties may arise during the financial statement review.

3. Evaluation of Major Transactions

Auditors analyze all significant transactions in the financial statements and identify possible errors or uncertainties that may affect the overall audit results. This stage is important for assessing the reliability of the presented information.

4. Verification of Company Actions

Auditors evaluate what measures the company has taken to ensure the accuracy of reporting and proper accounting in Hong Kong. They also check for all supporting documents, such as invoices, bank statements, and contracts.

5. Formation of the Audit Opinion

Based on the review, the auditor forms an opinion on the accuracy and reliability of the company’s financial statements. This opinion serves as a basis for assessing the company’s financial condition by tax authorities and other stakeholders.

6. Signing Reports and Submission to Tax Authorities

After completing the review, the audit reports and other documents are signed by the company’s directors and returned to the auditor. The auditor or tax agent then prepares the tax calculation and submits all these documents along with the PTR tax return to the Inland Revenue Department.

The audit process may include additional stages, such as account adjustments, responding to auditor inquiries, and clarifying details of financial transactions. However, this brief overview provides a basic understanding of how a company audit is conducted in Hong Kong.

Types of Audit Opinions

The company’s auditor is responsible for reviewing the financial statements prepared by the company’s directors. The auditor also prepares a report that includes the auditor’s expert opinion on the accuracy and reliability of the company’s financial statements.

1. Unqualified Opinion

The CPA confirms that the financial statements are prepared in accordance with accepted standards and do not contain significant errors.

2. Qualified Opinion

The auditor notes minor errors or deficiencies that require correction but do not undermine the overall accuracy of the statements.

3. Disclaimer of Opinion

The CPA believes that the financial statements are unreliable and cannot be used for decision-making by investors or creditors.

4. Adverse Opinion

The CPA cannot express an opinion because the documents were incomplete or key data was missing.

To conduct an audit, companies must provide the auditor with a complete set of documents that confirm all transactions and operations for the reporting period. These documents help the auditor assess the accuracy and compliance of the data presented in the financial statements.

List of Documents Required for Audit in Hong Kong

To ensure the audit is conducted correctly and timely, the company must prepare and provide the auditor with the following documents:

- Financial statements for the reporting period.

- Bank statements for all company accounts for the reporting period (including acquiring).

- Invoices and paid bills for purchases.

- Contracts (where applicable).

- Cash receipts, retail sales books (where applicable).

- Inventory data, stock balances (where applicable).

Frequently Asked Questions (FAQ)

Yes, even if a company does not conduct operational activities and does not engage in financial transactions, it is required to conduct an audit of zero reporting. In Hong Kong, the law requires all registered companies, regardless of activity, to annually submit financial statements confirmed by an auditor. This requirement is in place to prevent tax evasion and ensure transparency. Exceptions are companies that have obtained “dormant” status, but even in this case, a declaration is required.

To conduct an audit, companies must prepare a complete set of documents confirming all financial transactions for the reporting period. Key documents include bank statements for all accounts, contracts with partners and clients, purchase and sales invoices, expense receipts, as well as tax calculations and financial statements (balance sheet, income statement, cash flow statement). It is also important to provide accounting records and logs of all transactions so that the auditor can verify the accuracy of the presented data.

If a company fails to conduct an audit or submit audited financial statements within the established deadlines, it may face serious legal and financial consequences. The company may be fined up to 300,000 HKD, and additional sanctions may be imposed, such as blocking access to financial markets and restrictions on entering new contracts. In particularly serious cases, this may lead to the disqualification of directors and even the forced liquidation of the company if violations persist.

To obtain “dormant” company status, an application must be submitted to the Hong Kong Companies Registry. This is possible if the company is not actively conducting business and does not engage in financial transactions. Obtaining this status exempts the company from the requirement to undergo an annual audit and submit full tax reports. However, the company is still required to submit zero declarations and maintain a minimal amount of corporate documentation to confirm its status. Upon resuming activities, the “dormant” status must be revoked.

Yes, even if a company does not conduct commercial activities and has no financial transactions, it is required to submit a zero declaration. This is necessary to confirm to the tax authorities (IRD) that there were no taxable income and expenses during the reporting period. The zero declaration must be submitted on time, as failure to comply with this requirement may also result in fines. The IRD may request additional documents to confirm the absence of activity.