Hongkong

Hongkong China

China

Without a local account, settling with Chinese partners in renminbi is close to impossible — and banks have tightened their entry filter sharply in recent years. Here is what mainland banks check, which accounts a company can open, and how to clear the process without a rejection.

Why your company needs a bank account in China

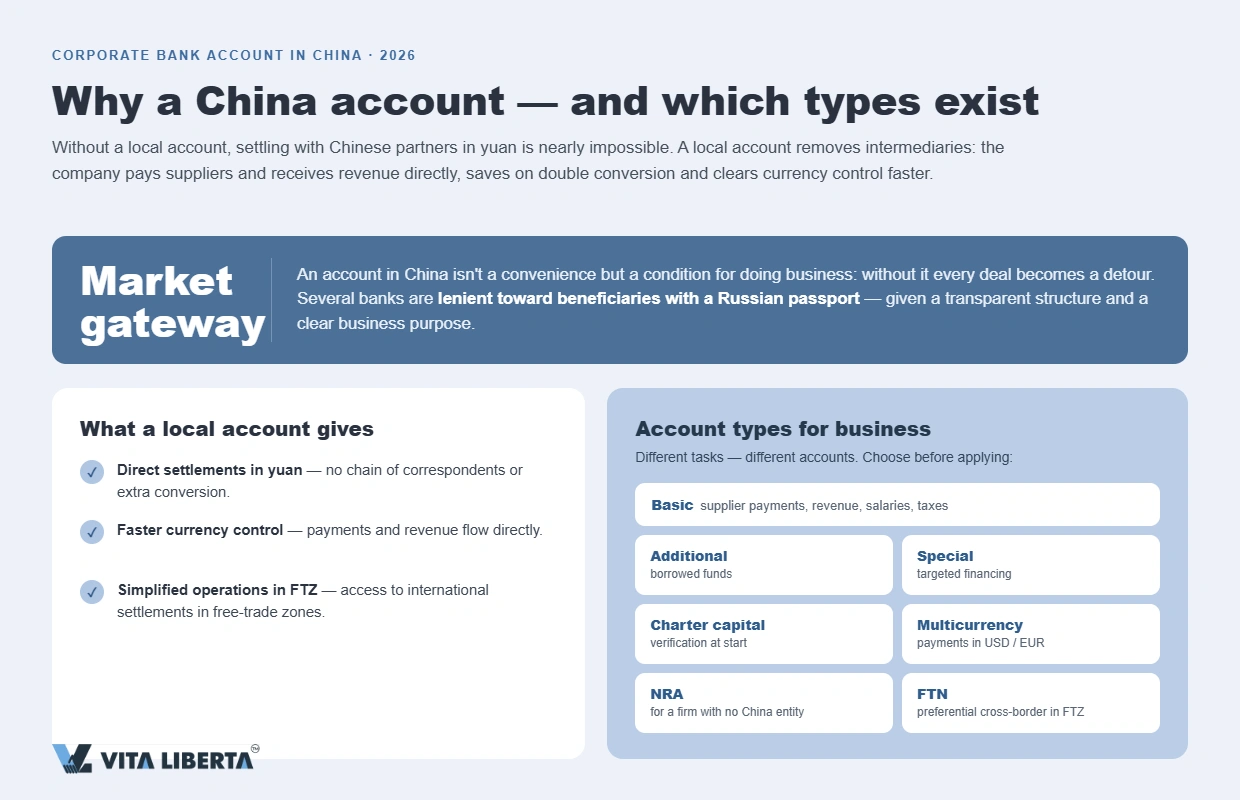

A local account removes the middlemen from your settlement chain: the company pays suppliers and receives revenue directly in RMB, avoids double conversion, and clears foreign-exchange control faster. For businesses in a free trade zone, it also unlocks simplified cross-border operations.

An account in mainland China is not a convenience — it is your entry ticket to the market. Without one, every deal turns into a detour.

It is also worth noting that a number of banks are relatively open to beneficial owners holding a Russian passport, provided the ownership structure is transparent and the business purpose is clear; on that basis, settlements with overseas counterparties run predictably.

What types of accounts companies open in China

Different tasks call for different account types, and the choice is best mapped out before you apply.

The basic account and supplementary accounts

The basic deposit account handles day-to-day activity: supplier payments, incoming revenue, payroll and taxes. As the business grows, companies add:

- general (supplementary) accounts to service borrowed funds;

- special-purpose accounts for earmarked financing and individual projects;

- a capital verification account at the start-up stage.

The more accurately you forecast future cash flows, the easier it is for the bank to build the right servicing structure.

Foreign-currency and NRA accounts for an overseas company

When a business needs to settle in dollars or euros, the bank sets up a multi-currency account. A company that does not yet have its own legal entity on the mainland can use the NRA format (Non-Resident Account). Banks are most willing to open these for Hong Kong companies, though Singapore, the UAE and the UK are also possible jurisdictions.

Here the bank scrutinises the economic substance more strictly: trade and logistics clear most easily. Inside free trade zones, an FTN-type account with lighter conditions for cross-border operations is also available.

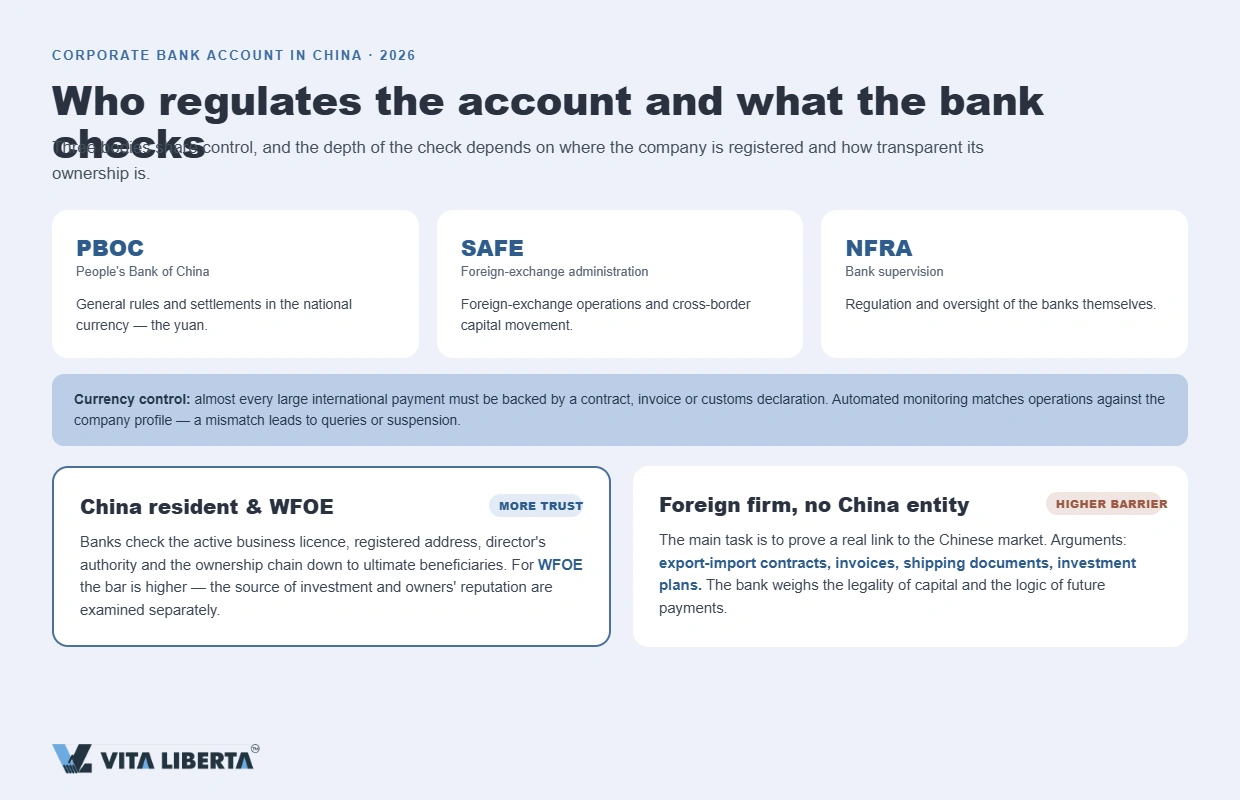

The regulators behind the account: what PBOC, SAFE and NFRA control

Three bodies share oversight. The People’s Bank of China (PBOC) sets general rules and local-currency settlement; the State Administration of Foreign Exchange (SAFE) handles foreign-exchange operations and cross-border capital movement; and supervision of the banks themselves sits with the NFRA.

Foreign-exchange control means that for almost every large international payment the bank will ask for supporting evidence — a contract, an invoice or a customs declaration. Automated monitoring reconciles transactions against the company’s declared profile, and any mismatch triggers queries or a suspension.

Bank requirements by company type

The depth of the review depends directly on where the company is registered and how transparent its ownership is.

PRC residents and WFOEs

Banks trust PRC-resident companies — including wholly foreign-owned enterprises (WFOEs) — most readily. The focus falls on a valid business license, the registered address, the scope of the director’s and representative’s authority, and the ownership chain up to the ultimate beneficial owners. The bar is higher for a WFOE: the source of the investment and the owners’ reputation are examined separately.

Foreign company with no PRC entity

This is where the barrier is highest. The main task is to prove that the company is genuinely tied to the Chinese market. Export-import contracts, invoices, shipping documentation and investment plans all serve as arguments. The bank decides case by case, weighing the legality of the capital and the commercial logic of the payments to come.

Struggling to open a bank account?

- Right bank for your business

- Full document package prepared

- Non-resident rules covered

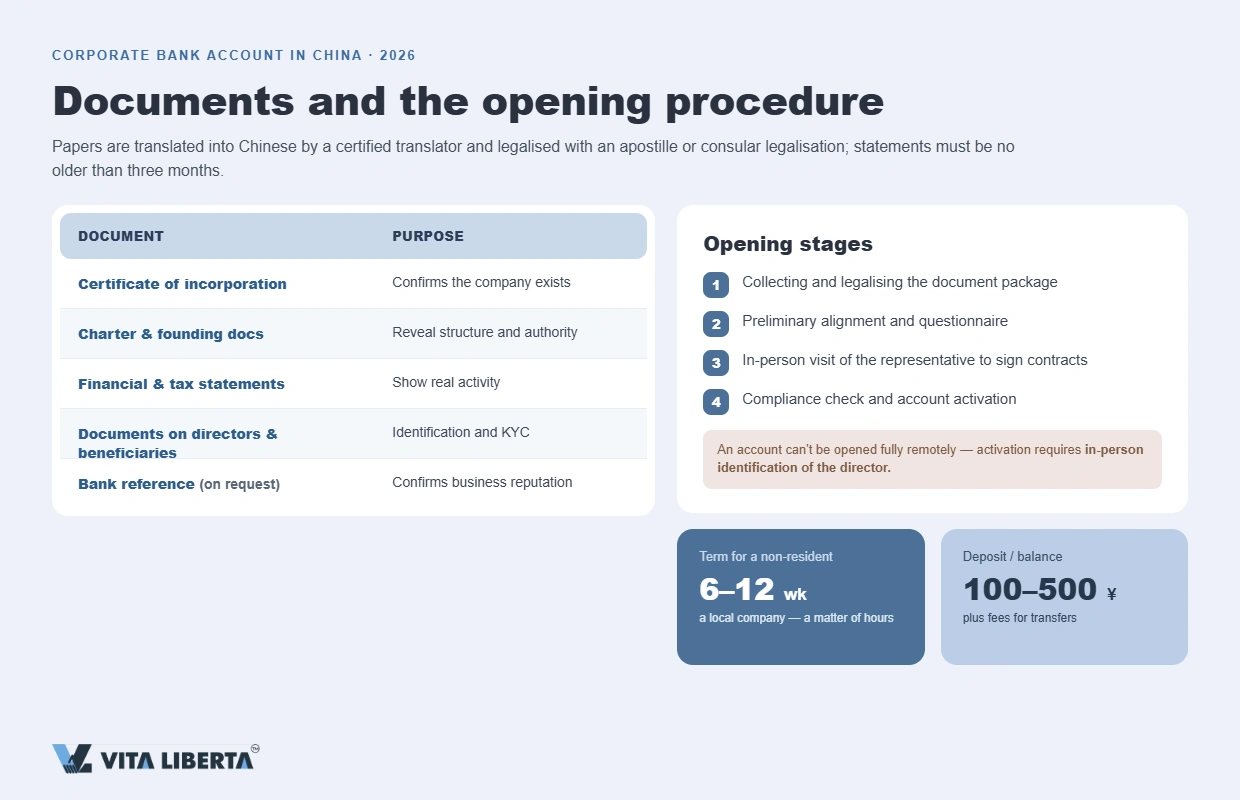

Which documents are needed, and how to legalize them

The standard package consists of registration and constitutional documents, accounting and tax filings, a description of the business, plus passports and address confirmations for directors and beneficial owners. Papers are translated into Chinese by a certified translator and legalized by apostille or, for non-Convention countries, by consular legalization; extracts must be recent — usually no older than three months.

| Document | Purpose |

| Certificate of incorporation | Confirms the company exists |

| Articles of association | Reveal structure and authority |

| Financial and tax filings | Show real activity |

| Director and UBO documents | Identification and KYC checks |

| Bank reference (on request) | Confirms business standing |

The opening procedure: stages, timelines and personal presence

Some banks accept preliminary scans remotely, but a corporate account cannot be opened fully online: activation requires in-person identification. The stages look like this:

- Collect and legalize the document package.

- Preliminary alignment with the bank and the application form.

- A visit by the legal representative to sign the agreements.

- Compliance review and account activation.

The director’s personal attendance is mandatory; a representative acting under a power of attorney is allowed less often. For non-residents the review takes six to twelve weeks on average, whereas a local company can be done within hours.

What it costs to open and maintain an account

Opening itself is inexpensive, but most banks that work with foreigners require a deposit and a minimum balance. Market reference points are a deposit of 100 to 500 RMB, plus fees on interbank and foreign-currency transfers. Each bank sets its own exact figures and balance threshold, so confirm the tariffs before you apply.

Why banks reject applications — and how to lower that risk

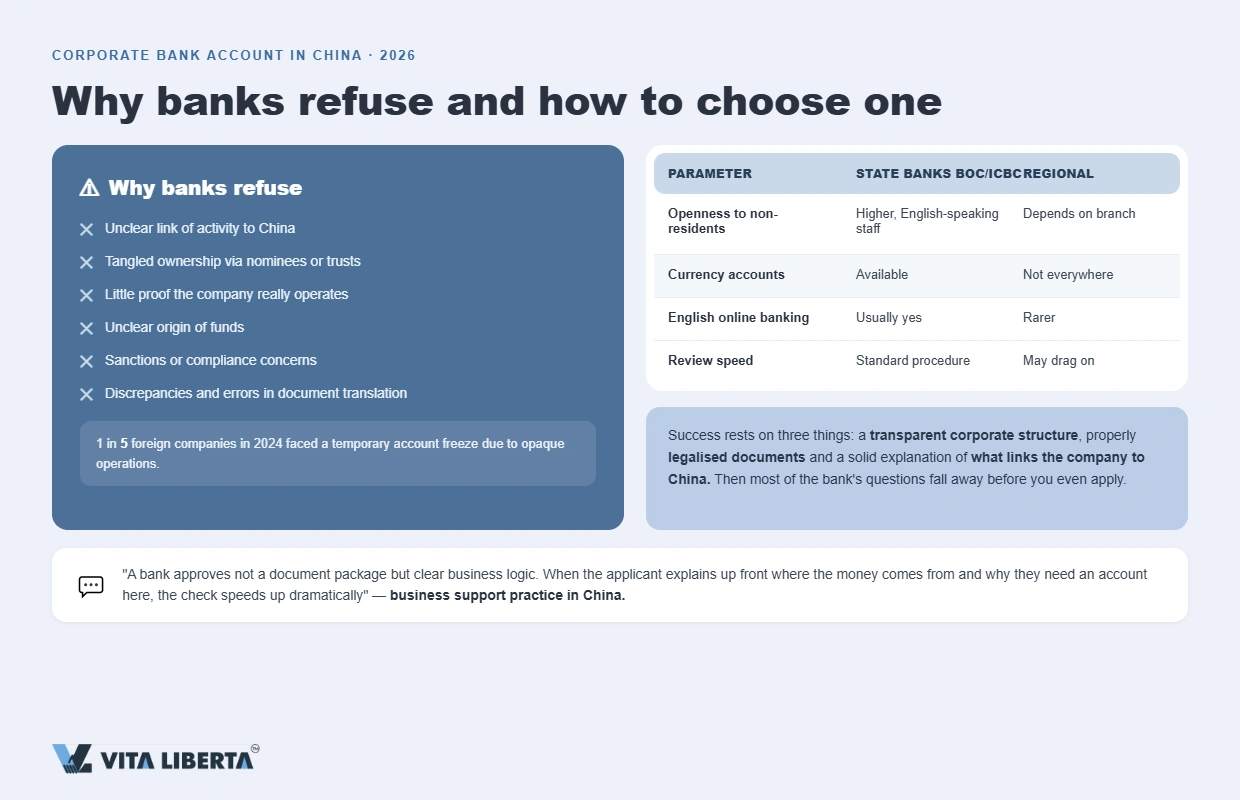

A negative decision almost never comes down to a single missing document; usually the bank is simply not prepared to accept that level of risk. The factors that most often work against an applicant:

- a weak link between the activity and China;

- ownership tangled through nominees or trusts;

- little evidence that the company genuinely operates;

- an unclear source of funds;

- sanctions or compliance sensitivity;

- inconsistencies and inaccuracies in the translated papers.

“A bank doesn’t approve a document package — it approves a clear business logic. When the applicant explains upfront where the money comes from and why they need an account here specifically, the review speeds up several times over,” notes partner in the China business-support practice.

By market estimates, one in five foreign companies faced a temporary account freeze in 2024 because of opaque transactions, so after opening it is important to keep documents updated and to confirm the purpose of large payments.

Choosing a bank in China: what to look at

Institutions differ in their openness to non-residents, their range of foreign-currency products, and the pace at which they process applications. It is safer to start with large banks that already have experience serving foreign clients.

| Parameter | Large state banks (BOC, ICBC) | Regional banks |

| Openness to non-residents | Higher; English-speaking staff available | Depends on the branch |

| Foreign-currency accounts | Available | Not everywhere |

| English online banking | Usually yes | Less often |

| Processing speed | Standard procedure | May drag on |

Tie your choice to the jurisdiction of your company and the nature of your operations — not just to the bank’s name recognition.

Takeaways

Opening a corporate bank account in China is realistic, but it is a project, not a formality. Three things decide the outcome: a transparent corporate structure, properly legalized documents, and a solid explanation of what connects the company to China. Check your own package in advance and state your business purpose clearly, and most of the bank’s questions fall away before you even apply.

Need a corporate account in China?

- Account opening support

- Handling foreign-exchange control

- Faster compliance approval

FAQ

Not entirely. Some banks will accept an application form and scans online, but the account can only be activated after the representative is identified in person at a branch.

Not always. A foreign company without a registration can open an NRA account, but it must prove a real connection between its activity and the Chinese market.

The usual reference is 100 to 500 RMB. The specific figure and the minimum-balance threshold are set by the chosen bank and account category.

Typically one and a half to three months once you factor in document legalization and compliance; a resident company moves through the process far faster.

The decision turns on the risk profile: no link to China, an opaque ownership structure, or questions about the source of funds outweigh formal completeness.