Hongkong

Hongkong China

China

Paying in US dollars means two conversions, extra correspondent banks and slower settlement. Pay your supplier in their own currency and the money often lands the same day — here’s how to make the switch cleanly.

Why pay in renminbi at all

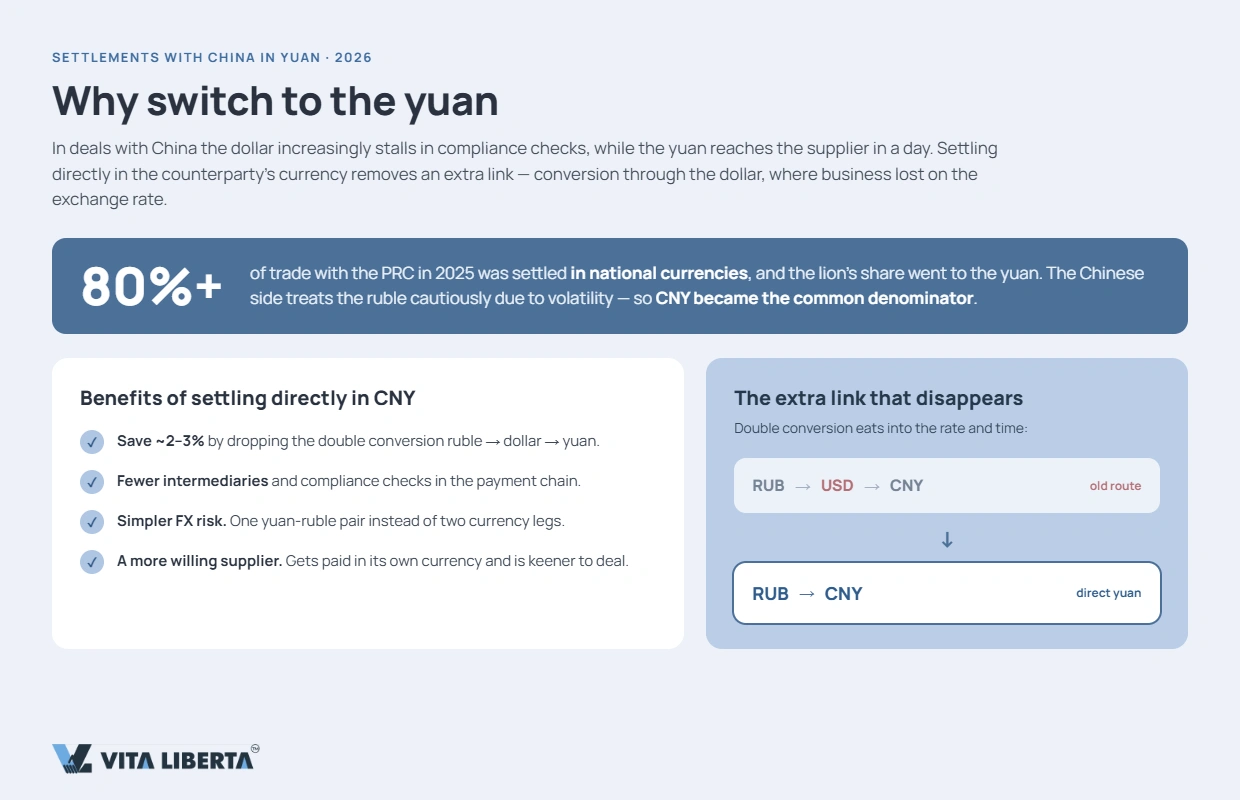

When you pay a Chinese supplier in USD, someone has to convert your currency to dollars and then dollars to renminbi. You lose margin on both legs, and every intermediary bank adds a fee and a compliance check. Settling directly in RMB removes that middle step. The gains are concrete:

- roughly 2–3% saved by dropping the double conversion — the PBOC itself estimates overseas importers who invoice in RMB save up to 3% in “hidden costs”;

- fewer intermediary banks and fewer compliance touchpoints;

- one currency pair to manage instead of two, which makes FX risk far easier to control;

- suppliers get paid in their own currency, so they quote sharper prices and negotiate more willingly (a USD quote usually bakes in an FX buffer to protect them).

Adoption has moved fast: around 30% of China’s trade is now settled in renminbi, up from roughly 10% in 2017. RMB has become the common denominator for cross-border trade with the mainland.

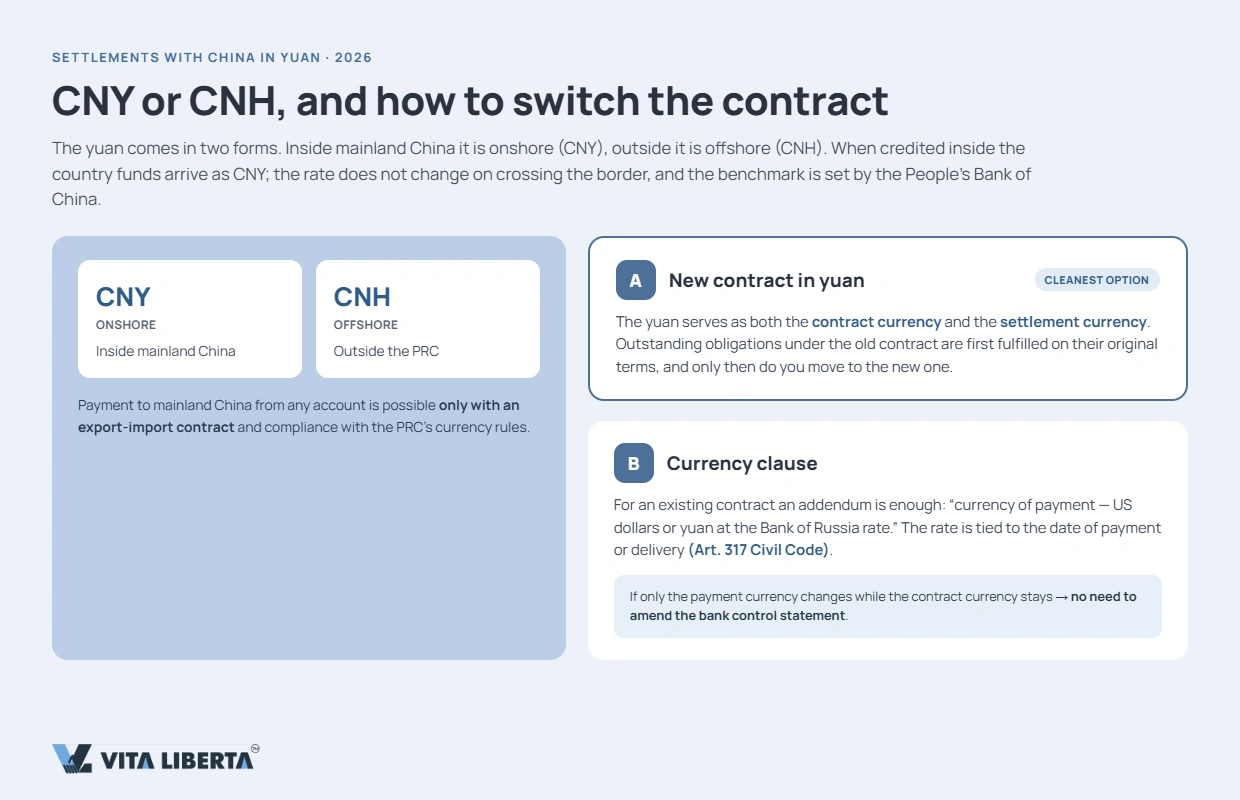

CNH or CNY: which one do you actually send?

Renminbi comes in two flavours. Onshore (CNY) trades inside mainland China; offshore (CNH) trades everywhere else — Hong Kong, Singapore, London. If you’re paying from outside the mainland, you send CNH. Your bank converts your local currency (or USD) into CNH, and when the funds cross into China they are booked to your supplier as CNY at a 1:1 rate — there’s no second conversion on arrival.

The catch is that they are not quite the same currency against the dollar. CNY is managed: the PBOC sets a daily central parity rate and onshore trading may only move within a ±2% band around it. CNH floats freely on international demand, so the two quotes drift apart. That gap is the spread, and it’s the first hidden cost of any cross-border RMB payment.

Step 1: fix the currency in the contract

Two clean routes exist.

A new RMB contract. The tidiest option is a contract where renminbi is both the contract currency and the settlement currency. If an older agreement still has open obligations, close those out on their original terms first, then move to the new one.

A currency clause. For a live contract, an addendum is enough. Add a payment clause along the lines of: “the currency of payment is USD or Chinese renminbi, converted at the agreed reference (mid-market) rate on the date of goods receipt.” You can peg the rate to the payment date or the delivery date. Keeping the contract currency unchanged while only switching the payment currency also keeps your bank’s trade-file paperwork simpler.

Want to switch to yuan settlements?

- Set up your CNY payments

- PRC currency controls covered

- Cut sanction and blocking risks

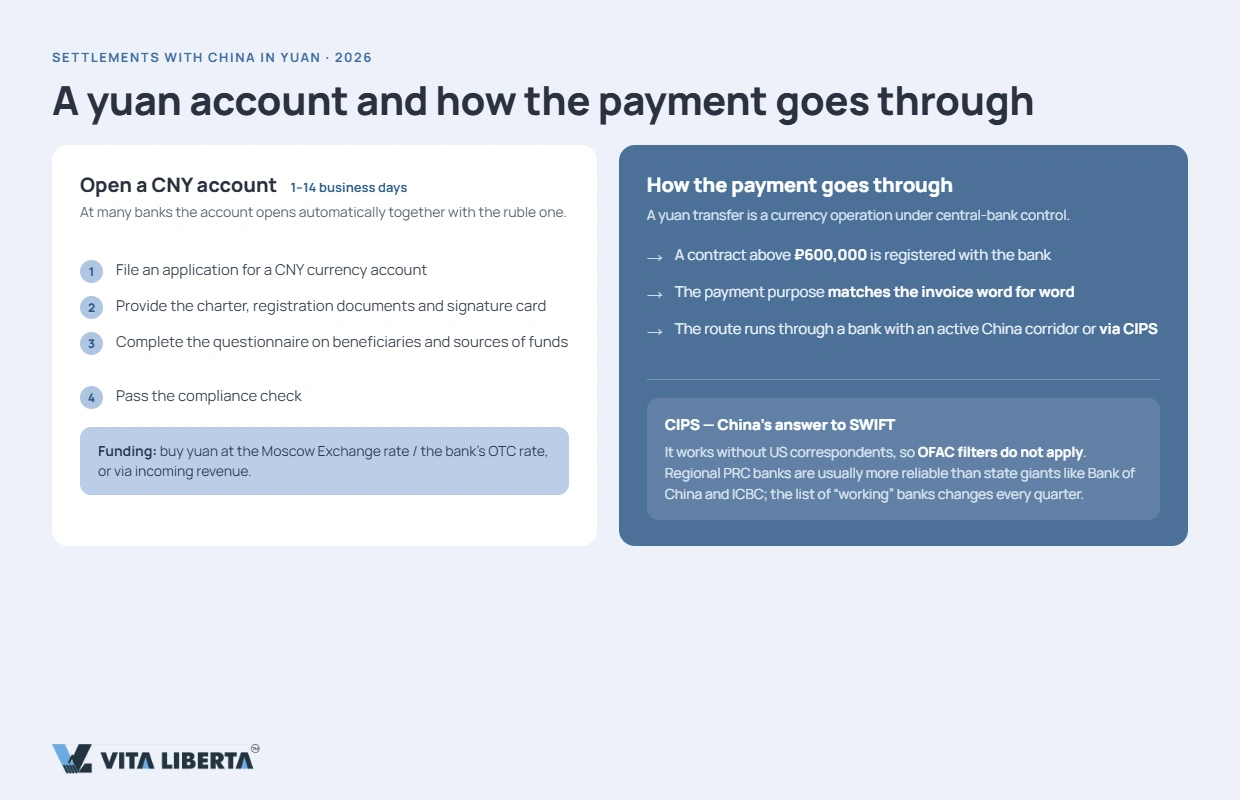

Step 2: open an RMB-capable account

For regular direct payments you need somewhere to hold and send CNH. A dedicated RMB account at a bank with a live China corridor works; so does a multi-currency business account (WorldFirst, Airwallex and similar) that lets you convert straight into CNH without hopping through USD.

Opening typically takes 1–14 business days. Expect to:

- apply for the CNH/foreign-currency account;

- supply your incorporation documents and signatory records;

- complete a beneficial-owner and source-of-funds questionnaire;

- pass KYC/compliance screening.

Fund the account by buying CNH at your provider’s rate, or from incoming RMB receivables.

Step 3: how the payment actually moves

An RMB transfer routes one of two ways: through a bank with an active China corridor, or through CIPS — the Cross-border Interbank Payment System, China’s own RMB clearing-and-settlement rail, launched in 2015 and overseen by the PBOC. CIPS clears RMB only and businesses can’t touch it directly; you reach it through a participant bank.

Two mainland-side requirements matter. Your supplier’s company must be registered in the RCPMIS (the PBOC’s cross-border RMB reporting system) before it can receive foreign RMB — usually a one-time registration by their bank. And every cross-border RMB payment needs a payment purpose code, so the description must match your invoice and contract word for word. On the conversion side, larger inflows draw SAFE review, and Chinese recipients document incoming funds with the authorities within a few days of receipt.

What it costs

| Route | Timing | Cost |

| USD through a correspondent chain | 5–10 days | 4–5% + risk of return |

| Direct RMB through a bank | 1–3 days | 1–2.5% |

| Payment agent | 1–3 days | 3–7% |

A direct RMB payment is the sender’s fee plus the receiving bank’s charge (roughly 20–80 CNY). Don’t forget the spread: the gap between buy and sell rates sometimes eats more than the visible fee.

⚠️ Get the payment description exactly right. The purpose/description on a cross-border RMB payment must mirror the invoice and contract precisely. A vague “for goods” is one of the most common reasons a transfer bounces.

Risks and how to contain them

A payment can stall over the sanctioned status of a party, unexplained amounts above a threshold, or ordinary compliance queries. You cut the odds by choosing a bank with a stable China corridor, keeping documents clean, writing a currency clause into the contract, lining up a backup route in advance, and validating any large transfer with a small test transaction first.

“Switching to RMB isn’t ‘change USD to CNH in the payment field.’ First the contract and the account, then clean, matching documents, and only then the channel. Companies that take these steps in order get steady payments and real savings — not returns.”

— Sergey Konon, cross-border trade (China) specialist

The bottom line

Moving to RMB settlement comes down to four moves: amend the contract with a currency clause (or sign a new one), open a CNH-capable account, prepare documents that match to the letter, and pick a working channel. Add it up and RMB is cheaper and more predictable than a dollar chain. Start with the contract and the account, get the payment purpose right — and payments to your partner stop bouncing.

Ready to pay Chinese partners?

- We process your yuan payment

- Bank and settlement scheme picked

- Full FX transaction support

FAQ

From outside mainland China you send CNH. Your bank converts your currency into offshore renminbi (CNH), which is booked to your supplier as onshore CNY at 1:1 once it lands in China. You never send CNY directly from abroad.

RMB routes skip the extra USD conversion and one or more correspondent banks, so there are fewer points where a payment can be delayed or marked up. The amounts in your contract, invoice and payment also line up, and suppliers who don’t have to hedge FX often quote lower prices.

For regular corporate payments it’s the most practical option. Alternatively a licensed payment provider can take your local currency, convert to CNH and deliver CNY to your supplier — saving you the double exchange.

No. SWIFT is a messaging network that carries payment instructions; CIPS is a payment system that clears and settles cross-border transactions in RMB. Businesses can’t access CIPS directly — you reach it through a participant bank.

Usually the FX rate moving between quote and payment, compliance checks at the Chinese bank, or errors in the payment details — a purpose/description that doesn’t match the invoice is a classic cause. Fix the rate early, keep documents tidy, and use proven channels.