Hongkong

Hongkong China

China

Registered Capital, as stipulated in the company’s constitutional documents and recorded in the register of the State Administration for Market Regulation (SAMR), is not merely a formal figure. It represents a legal obligation of the founders towards the company and its creditors, a fundamental guarantee of the financial soundness of the business entity. The requirements for its contribution in China have undergone a significant transformation, reflecting the pendulum of state policy between stimulating entrepreneurial activity and protecting market stability.

Historical Context and Essence of the 2024 Changes

Before 2013, China operated under a system requiring founders to contribute capital within strictly defined timelines and with minimum thresholds. The liberal reform of 2013 abolished both the deadlines and minimum amounts for most industries, transferring the process to the discretion of shareholders. This led to a boom in company registrations but also gave rise to risks associated with “shell” companies. The new revision of the PRC Company Law, which came into effect on July 1, 2024, marks a return to a regulated model, but in an updated format. The key innovation is the reinstatement of a fixed maximum term for the full payment of the registered capital. According to the amendments, founders are obligated to fully fulfill their financial obligations, as stipulated in the company’s articles of association, within 5 years from the date of the company’s state registration. This rule is mandatory and aims to strengthen the creditworthiness of businesses from the moment of their establishment.

Critical Aspects of the New Legal Regime for Registered Capital Contribution in China

The five-year limit applies to all forms of limited liability companies and joint-stock companies, unless otherwise expressly stipulated by special laws or regulations of the State Council of the PRC for organizations in highly regulated sectors (financial institutions, insurance companies, securities firms, etc.).

The 5-year principle now also applies to capital increase procedures. For an increase registered on or after July 1, 2024, the countdown for making the additional contributions begins from the date of registering the corresponding changes with SAMR.

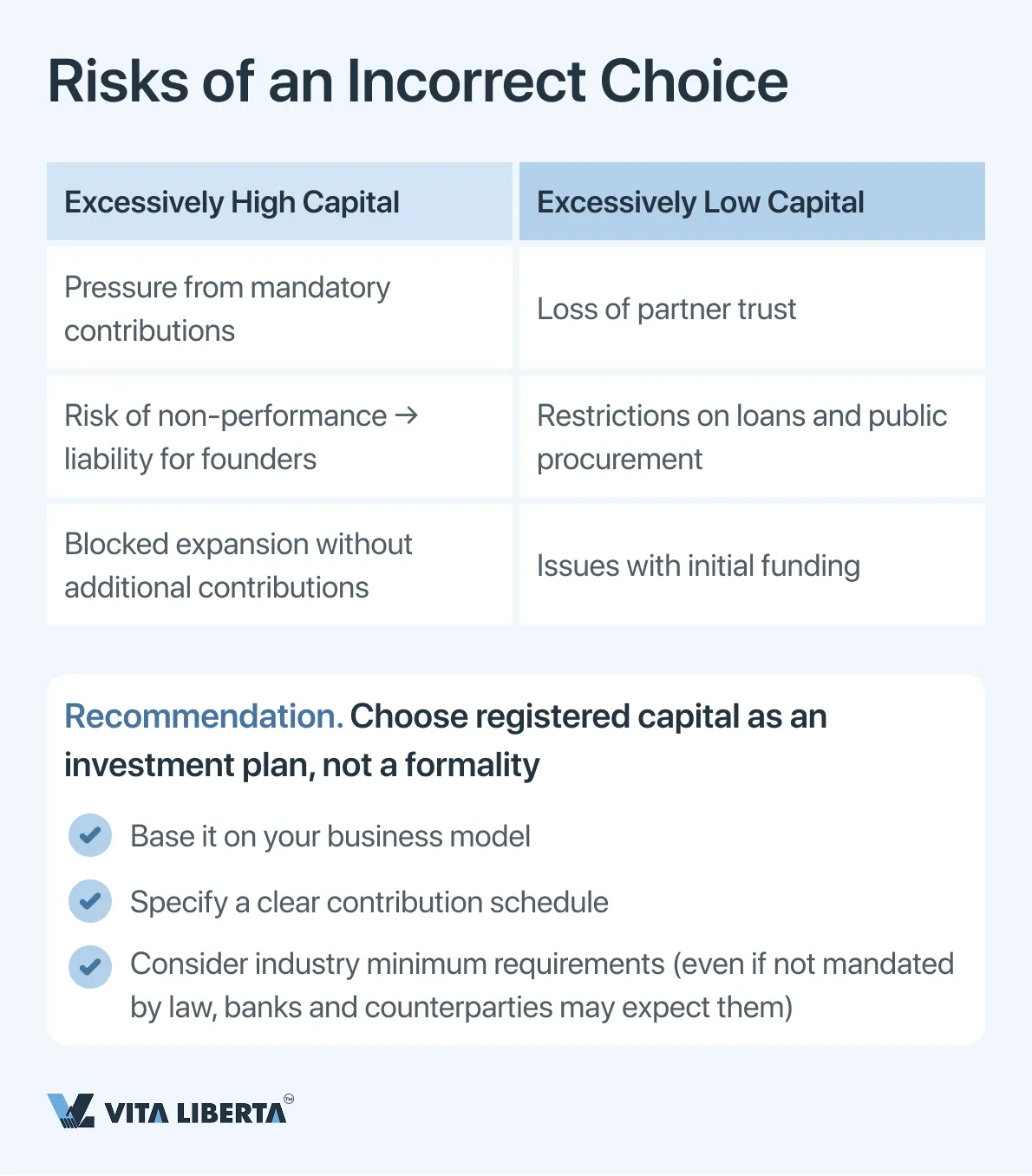

This change transforms the planning approach. The registered capital amount ceases to be a nominal figure “for the future.” It now demands a well-considered calculation based on realistic financial forecasts and a scheduled investment plan for the upcoming five-year horizon. Overestimating the figure can create an unsustainable financial burden, while underestimating it can undermine partner trust, limit opportunities for raising debt financing, and restrict funding for the company in its early development stage.

Transitional Provisions for Existing Companies

The legislators have provided a flexible adaptation mechanism for companies registered before the amendments took effect. A transition period has been established for them, aimed at gradually bringing their capital structure into compliance with the new standards.

Such companies will need to develop and approve an adjusted capital payment schedule that fits within the remaining period until the expiration of 5 years, counted from July 1, 2024. Specific methodologies and deadlines for submitting adjusted schedules are to be detailed in subsequent regulations from SAMR.

Exception for “Mature” Companies: Companies whose registered capital was already fully paid up by July 1, 2024, are not subject to the new deadlines. For them, the previous regime remains in effect.

Thus, the new legal regime underscores that registered capital in modern Chinese corporate law is not a passive registry entry, but a dynamic tool for financial planning and an indicator of shareholder seriousness. It requires a responsible and strategic approach throughout the entire lifecycle of the company.

Legal Architecture of the Transition Period and Strategic Management of Registered Capital in Light of the 2024 Reform

The corporate law reform, which took effect on July 1, 2024, includes not only new rules for newly established companies but also a complex adaptation mechanism for millions of existing enterprises. The key document detailing this process is the State Council Regulation on the Implementation of the Paid-in Registered Capital System, which establishes a differentiated and phased transition regime.

Detailing the Transition Period: From Declarative to Mandatory Implementation

The legislator has provided asymmetric approaches for different business forms, acknowledging their distinct nature and the varying responsibilities of founders.

| Company Type | Registration Date | Transition Period Requirements | Strategic Task for the Company |

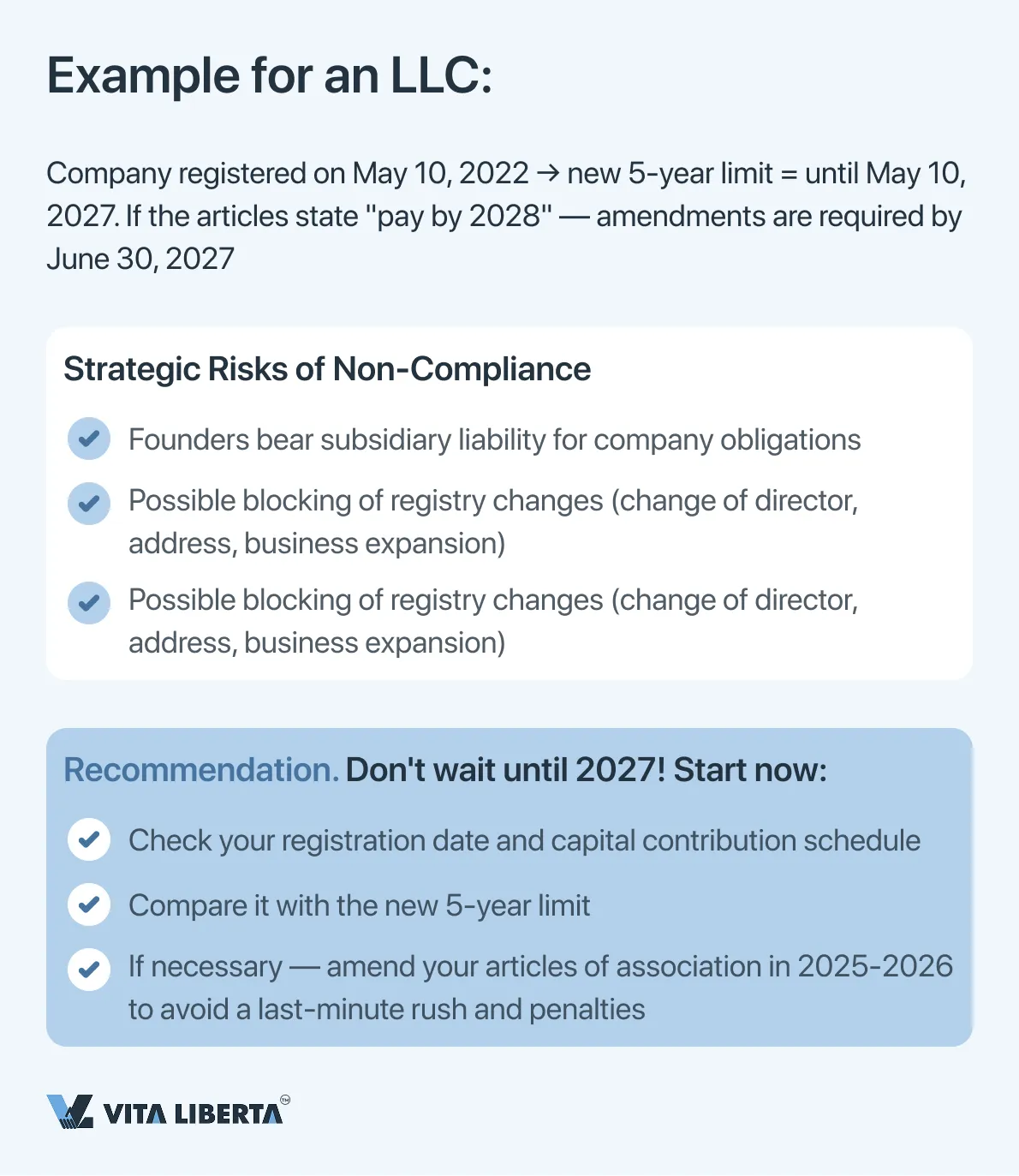

| Limited Liability Companies (LLCs) | Before July 1, 2024 | 3-year grace period (July 1, 2024 – June 30, 2027) to align the payment schedule with the 5-year rule, counted from the registration date. | 1. Schedule Analysis: Compare existing payment obligations with the new 5-year limit from the registration date. 2. Adjustment: If the remaining payment period under the old articles of association extends beyond July 1, 2029 (5 years from the final date of the transition period), it is mandatory to amend the articles and register a new schedule with SAMR by June 30, 2027. |

| Joint Stock Limited Companies (JSCs) | Any date before July 1, 2024 | Hard Deadline: Founders (promoters) must fully pay for all subscribed shares by June 30, 2027, regardless of prior agreements. | Aligning the financial obligations of founders with the new standards within a tight timeframe, which may require significant reorganization of internal cash flows. |

Important nuance: For LLCs whose existing payment schedule already fits within the new 5-year limit (counted from their original registration date), formally amending the articles of association is not required. However, conducting an internal audit and obtaining confirmation of compliance is recommended.

We’ll Help You Set the Right Registered Capital in China

- Capital calculation for your business model

- Payment deadline & risk assessment

- FIE structure support

Procedure for Amending Registered Capital: From Rigid Control to Subsidiary Liability

The company’s right to increase or decrease its registered capital remains, but it is now framed by a set of sanctions for procedural violations, which have been significantly strengthened.

- Legal Procedure as a Guarantee for Creditors.

Any change in capital requires:

• A decision by the highest governing body (general meeting of shareholders/participants).

• Notification of creditors within the statutory timeframe and granting them the right to demand early fulfillment of obligations or the provision of security (in the case of a capital decrease).

• Registration of the changes with SAMR, providing proof of payment (for an increase) or evidence of proper creditor notification (for a decrease).

2. Categorical Prohibition and Its Consequences: “Piercing the Corporate Veil.”

It is critically important that the illegal withdrawal of contributed capital (e.g., through sham transactions, interest-free loans to founders, or returning contributions under false pretenses) is no longer considered a mere administrative violation. This action is now qualified as an abuse of the company’s separate legal status to harm the interests of creditors.

The consequences are personal and severe:

- Subsidiary Liability of Founders (Shareholders): Creditors obtain the right to recover the company’s unpaid debts directly from the liable founders, bypassing the company’s limited liability (“piercing the corporate veil”). This is a fundamental blow to a core principle of corporate law.

- Joint and Several Liability of Management: Directors, supervisors, and senior management who authorized, facilitated, or failed to prevent such a withdrawal bear joint and several liability to the creditors. This makes the corporate officer’s position personally risky for non-compliance with corporate financial norms.

Strategic Business Implications

Audit and Planning are Top Priority. All companies registered before July 2024 must conduct an audit of their registered capital and payment schedule, comparing them with the new norms. For LLCs, this is a matter of strategic scheduling; for joint-stock companies, it is a matter of urgent full payment.

Capital is Not Founders’ Personal Asset. Robust internal financial controls must be established to eliminate any transactions involving contributed capital that could be interpreted as its covert withdrawal. Dividends and shareholder loans must strictly comply with the law and the company’s genuine financial capacity.

Risk Has Become Personal. The new rules explicitly shift the consequences of financial abuse from the realm of corporate risk to that of personal financial catastrophe for founders and top managers. Procedural compliance is the only safeguard for personal assets.

Thus, the transition period is not merely a technical grace period but a strategic window of opportunity to legitimize and optimize the capital structure for the new reality. In this reality, transparency and the timely contribution of capital have become critical factors not only for business reputation but also for the personal financial security of the company’s beneficiaries.

Forms of Registered Capital Contribution: Strategic Choice of Assets Within the Legal Framework of the PRC

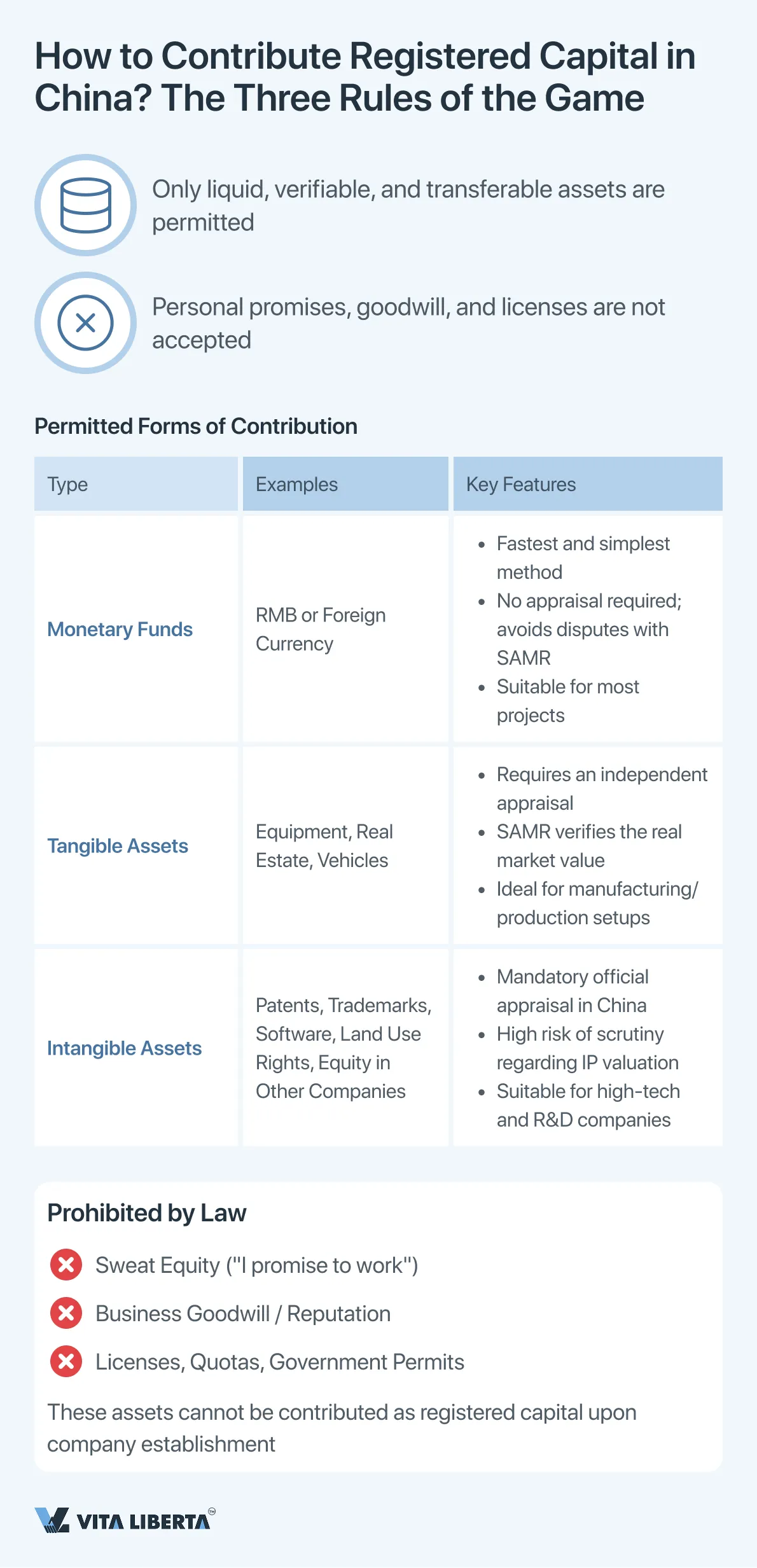

Contributing to the registered capital of a Chinese company provides investors with flexible options for structuring initial assets. However, this choice is strictly bounded by a legal framework designed to ensure the contributed value is real, liquid, and verifiable, thereby protecting creditor interests and market stability.

Monetary Contribution: Efficiency and Unconditional Acceptance

A cash contribution (in RMB or foreign currency) is the most predictable and straightforward method. It does not require additional appraisal procedures, minimizes registration timelines, and eliminates subjectivity during SAMR review. For foreign investors, it also represents the most transparent route for currency conversion and cross-border fund transfers.

Non-Monetary Contribution: Opportunities and Regulatory Complexities

The law permits in-kind contributions, provided they meet two key criteria:

- Objectively Appraisable: The asset must have a documented, verifiable market value.

- Legitimately Transferable: Ownership or use rights must be lawful and capable of being transferred to the company without encumbrance.

Permitted assets include:

• Tangible Assets: Production equipment, real estate, vehicles.

• Intangible Assets:

• Land Use Rights.

• Intellectual Property: patents, trademarks, software copyrights, protected know-how.

• Equity interests in other companies.

• Creditor’s Rights, assigned via contract.

For any non-monetary contribution, a report from a licensed Chinese appraiser is mandatory. SAMR scrutinizes the valuation justification for technologies and IP with particular rigor, requiring detailed descriptions and proof of future economic benefit for the company.

Categorically Inadmissible Forms of Contribution

The law excludes assets whose value is inseparable from the investor or which are not freely transferable:

• Sweat Equity: Promises of future labor, management services, or provision of time.

• Goodwill: Cannot be contributed as a standalone asset during company formation.

• Administrative Permits: Licenses, quotas, or government approvals—these are not objects of civil rights and cannot be transferred as contributions.

Comparative Analysis for Strategic Decision-Making

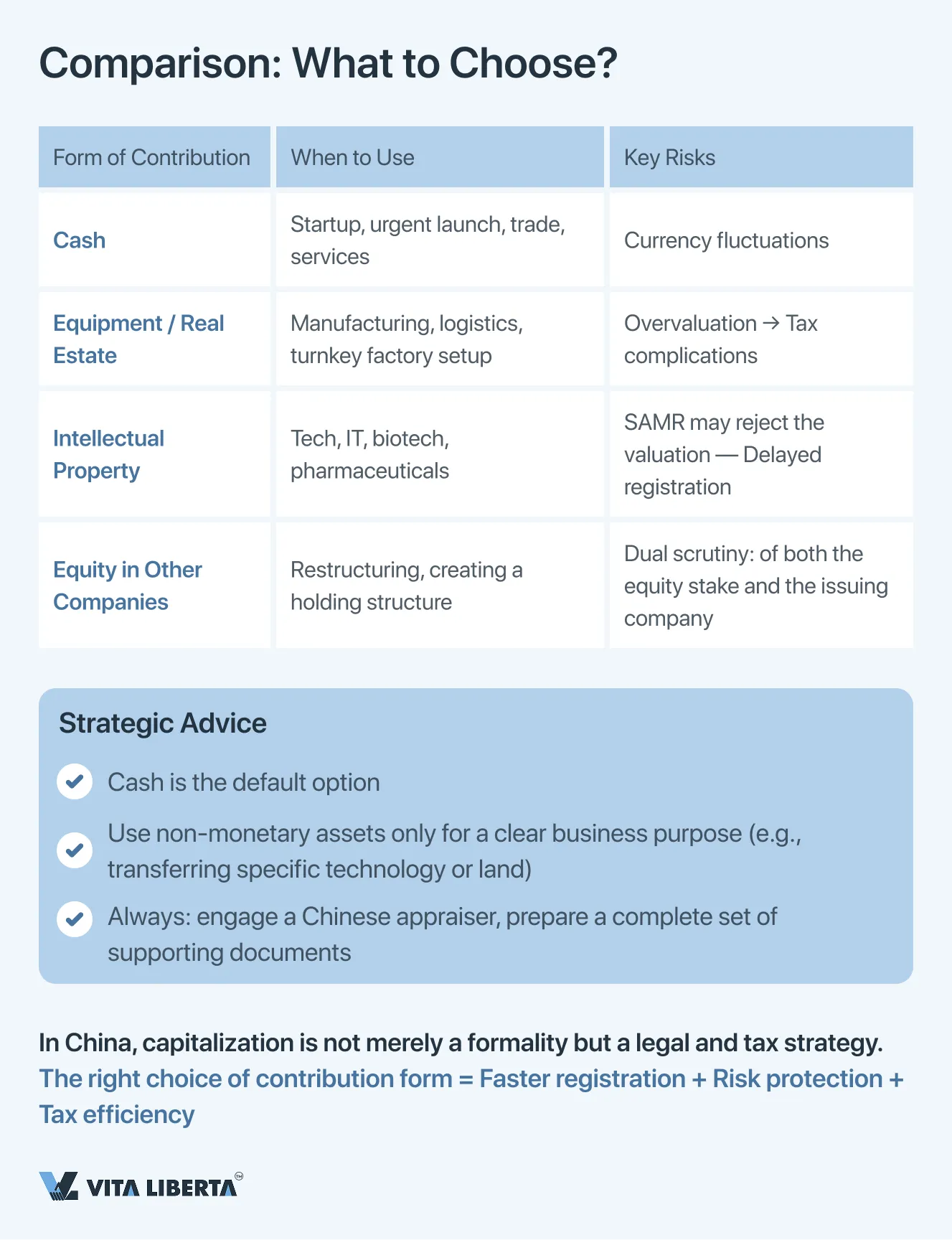

| Form of Contribution | Key Advantage | Primary Risk | Ideal Use Case |

| Monetary Funds | Speed and simplicity of registration. | Currency risk for the investor.. | Startups, projects requiring rapid launch of operations. |

| Equipment / Real Estate | Immediate company outfitting without additional procurement. | Risk of overstated book value and subsequent accelerated depreciation. | Establishing a production/manufacturing enterprise with specific technological assets. |

| Intellectual Property | Capitalization of R&D, creation of royalty streams for the rightsholder. | High risk of SAMR rejecting the valuation, difficulty in documentary substantiation. | High-tech sector projects where core value lies in patents or unique software. |

| Equity in Other Companies | Asset consolidation, restructuring of a corporate group. | Dual scrutiny (of the issuer company’s activities and the fairness of the equity valuation). | Integrating existing Chinese assets into a new holding structure. |

Choosing the form of contribution involves a balance between strategic objectives (company outfitting, tax optimization, consolidation) and the goal of minimizing administrative and legal risks. A non-monetary contribution, despite its appeal, transforms the registration process into a longer and more complex one, requiring the engagement of local experts for independent appraisal and legal support.

Disclosure of Registered Capital Information: Transparency as a Mandatory Element of Corporate Governance

As part of the effort to strengthen oversight of registered capital’s authenticity and protect creditor interests, new PRC legislation has introduced strict and timely requirements for the public disclosure of relevant information. This obligation is not a formality but a key element of the corporate accountability and public trust system.

Disclosure System: Centralized Public Registry

The primary platform for disclosure is the National Enterprise Credit Information Publicity System (accessible at www.gsxt.gov.cn). This resource serves as a unified public dossier for companies, accessible to counterparties, financial institutions, investors, and regulatory bodies.

The legal basis for disclosure is the Implementing Provisions of the Company Law, which obligate companies to enter up-to-date data into the system within specified deadlines.

Content and Deadlines for Disclosure: Timeliness and Accuracy

A company is required to disclose information within 20 working days after the occurrence of any of the following events:

| Change Category | Specific Data to Disclose | Practical Significance for Third Parties |

| Scope of Obligations & Fulfillment | Changes in the subscribed and paid-in capital amounts. | Allows assessment of the gap between obligations and their fulfillment, indicating financial reliability. |

| Asset Structure | Changes in the form of capital contribution (cash, equipment, intellectual property, etc.). | Provides insight into the liquidity of the company’s assets and its balance sheet structure. |

| Financial Schedule | Adjustments to the capital contribution schedule (e.g., under the transitional provisions). | Enables forecasting of the company’s future cash flows and assessment of default risks. |

| Shareholder Structure | For joint-stock companies – changes in the number of subscribed shares. | Reflects changes in the distribution of stakes and shareholder obligations. |

Strategic Implications and Risks of Non-Disclosure

The public nature of the gsxt.gov.cn system turns timely disclosure into a tool for business reputation and risk management.

- For Partners and Clients: It is the primary source for verifying a counterparty’s credibility. Outdated or contradictory information about capital immediately undermines trust and can be grounds for refusing to enter into a transaction.

- For Banks and Creditors: Financial institutions are required to check system data when reviewing loan applications. Disclosure violations or negative information can lead to funding rejection or stricter lending terms.

- For Regulators (SAMR, Tax Authorities): Discrepancies between a company’s internal documents and publicly disclosed information are a direct reason for unannounced inspections, fines, and inclusion of the company on an enhanced monitoring list. Failure to disclose on time or providing false information results in the company being added to an “abnormal operations list,” which blocks numerous administrative procedures, restricts participation in public procurement, and damages its reputation.

In the modern Chinese market landscape, the obligation to disclose registered capital information has evolved from a bureaucratic formality into a strategic function for managing reputation and legal risks. Maintaining complete, accurate, and up-to-date information in the public system is a continuous process that directly impacts a company’s operational viability, investment appeal, and creditworthiness. Regular auditing of one’s own data on gsxt.gov.cn should become a standard corporate governance procedure.

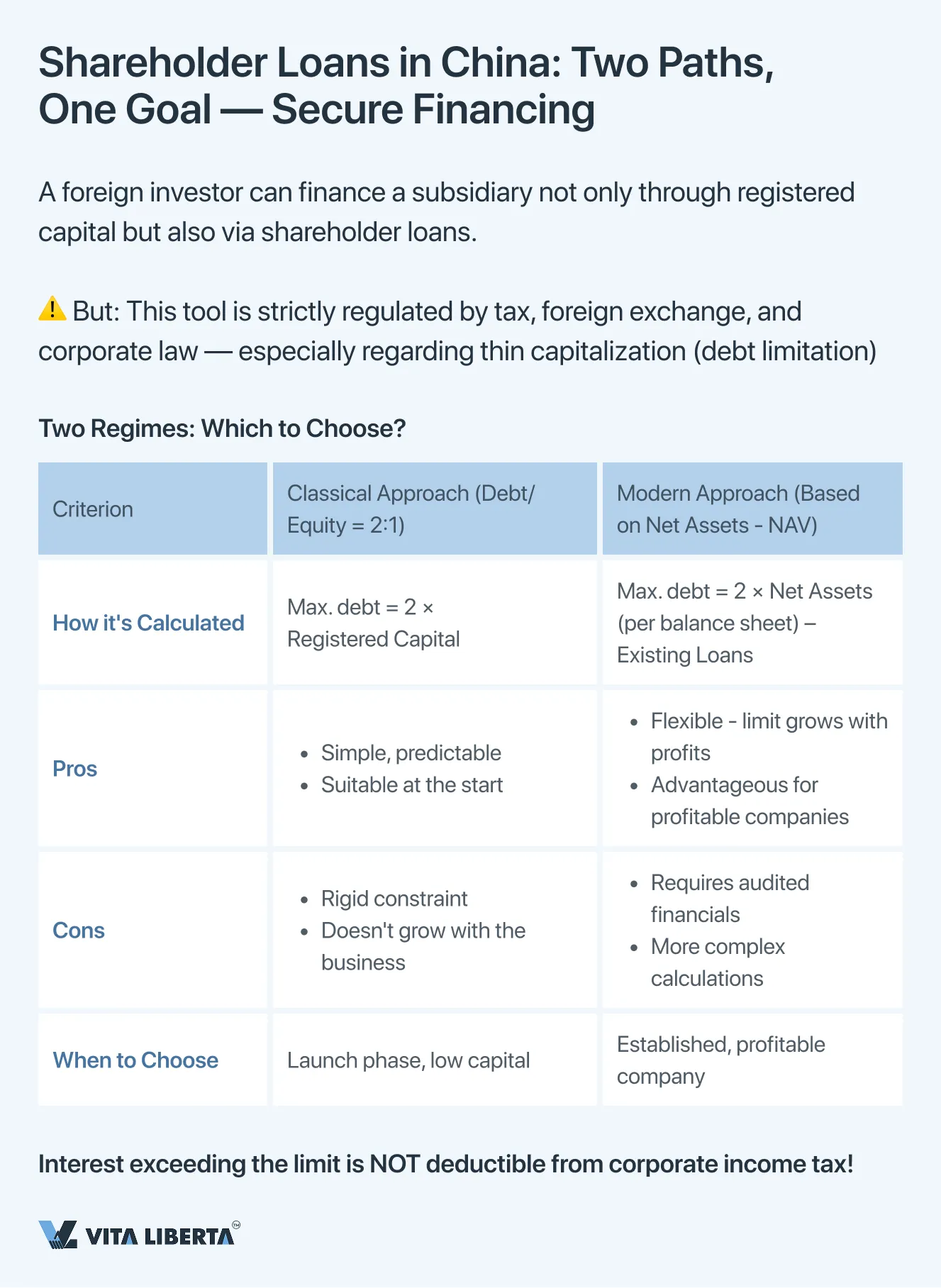

Shareholder Loans as a Financing Tool for Foreign-Invested Enterprises in China

In addition to contributing registered capital, a foreign investor possesses a significant tool for additional financing of its Chinese subsidiary: shareholder loans. This mechanism allows for flexible management of a project’s liquidity. However, it is strictly regulated by corporate, foreign exchange, and critically, tax law norms aimed at preventing base erosion (thin capitalization rules).

Two Regulatory Regimes for Debt Financing: Classical vs. Modern Approach

The legislation provides companies with a choice between two primary methods for calculating the permissible volume of shareholder loans, necessitating strategic tax planning.

| Regulatory Regime | Essence and Mechanism | Practical Application and Limitations |

| Classical Approach: Fixed “Debt-to-Equity” Ratio | Establishes a direct maximum ratio between shareholder loans and equity capital (most commonly 2:1 for manufacturing enterprises). Tax Consequence: Interest on loans exceeding the established limit is not recognized as an expense for corporate income tax calculation purposes in China. | Simplicity and Predictability. Easy to calculate and understand at the project’s outset. Inflexibility. Does not account for the actual scale and profitability of the business, potentially artificially restricting financing for growing companies. |

| Modern Approach: Tied to Net Asset Value (NAV) | The permissible volume of shareholder loans is tied to the company’s equity capital (net assets), calculated based on its financial statements. Formula: Permissible Loan = Net Assets x Coefficient (often 2) – Existing Shareholder Loans. | High Flexibility. Allows increasing the borrowing limit as the company grows and becomes capitalized, which is particularly advantageous for profitable enterprises. Dependence on Reporting. Requires quality audits and official confirmation of the net asset amount, complicating the process. |

Key Recommendation: Choosing the optimal regime is a strategic tax decision that must be made during the project’s financial modeling phase. It directly impacts:

- Tax Burden: The ability to deduct interest from the taxable base.

- Balance Sheet Structure: The debt-to-equity ratio.

- Cost of Financing: The actual effective interest rate on provided loans.

Consulting with a Chinese tax advisor to conduct a comparative analysis and formally document the chosen method in the company’s records is mandatory.

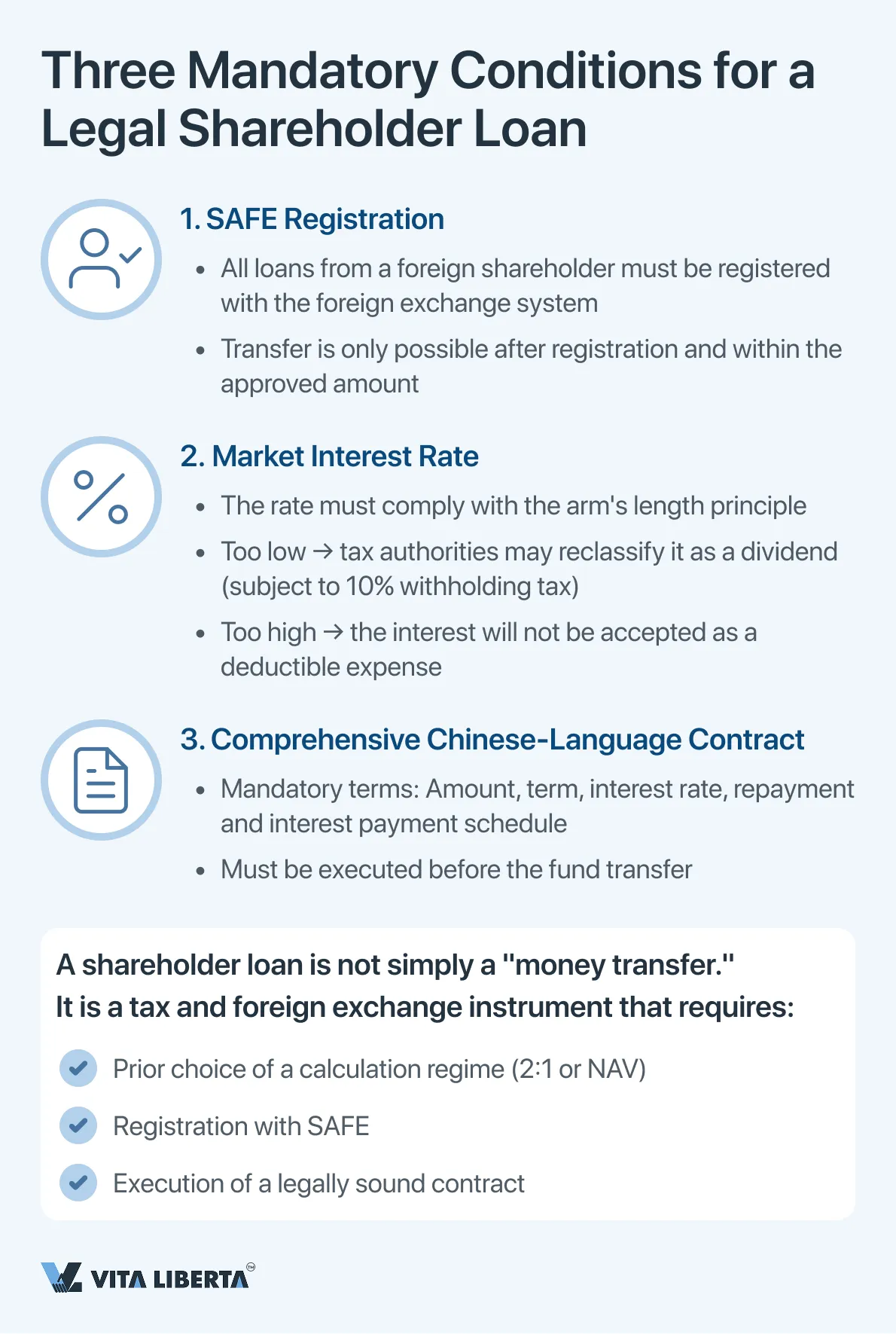

Critically Important Additional Conditions

- Foreign Exchange Regulation. All shareholder loans from a foreign investor are subject to registration with the foreign exchange control system (SAFE). Actual fund transfer is only possible after completing this registration and strictly within the registered amount. Violations result in severe fines and blocked transactions.

- Arm’s Length Interest Rate. The interest rate set for the loan must align with the market rate for comparable debt instruments. Rates set too low may be reclassified by tax authorities as a disguised dividend payment (subject to withholding tax), while rates set too high may be deemed unjustified expenses.

- Proper Documentation. The loan must be formalized with a comprehensive credit agreement in Chinese, clearly defining the amount, term, interest rate, interest payment method, and repayment schedule.

Shareholder loans are a powerful yet complexly regulated instrument. Their effective use requires not only investor liquidity but also an integrated approach combining corporate financing, tax optimization, and strict compliance with foreign exchange laws. Properly structured debt enhances a project’s financial efficiency, while planning errors can lead to significant fiscal losses and administrative risks.

Key Principles for Foreign Investors: A Memorandum on Registered Capital in the PRC

Registering a company in China requires a clear understanding and strict compliance with the rules for forming registered capital. Remember these five foundational points to minimize risks and launch your business successfully.

| Aspect | Core Principle | Practical Advice |

| 1. Payment Deadline | 5 years from the registration date is a firm rule for new companies (after July 1, 2024). For existing ones — a transition period until June 30, 2027 to align schedules. | Calculate the capital amount based on a realistic 5-year financing plan. Do not inflate the figure “just in case.” |

| 2. Obligation, Not Option | Contribution is not a right, but a duty. Delays lead to fines, operational restrictions, and inclusion on the public “abnormal operations list” on gsxt.gov.cn. | Treat declared capital as a legally binding financial commitment. |

| 3. Forms of Contribution | Permitted: Cash (best), equipment, IP, land use rights, equity in other firms. Prohibited: Labor, goodwill, promises, licenses. | Prefer cash contributions. Any other asset requires mandatory independent appraisal in China. |

| 4. Inviolability of Capital | Illegally withdrawing contributed capital is forbidden. This leads to “piercing the corporate veil”: founders and directors bear personal (subsidiary) liability for company debts. | Contributed funds are company property. Returns to the investor are only possible as dividends or through a legal capital reduction. |

| 5. Public Disclosure | Any change in capital (amount, form, schedule) must be disclosed on gsxt.gov.cn within 20 working days. This is the foundation of your public reputation. | Appoint a person responsible for regularly updating data in the system. Banks and partners check this information first. |

| 6. Alternative Financing | Shareholder loans are possible but subject to caps (2:1 ratio or NAV-based model). Interest exceeding the cap is not deductible for corporate income tax. | Consult with a tax advisor in advance to determine the optimal debt financing model for your project. |

Modern Chinese corporate law makes registered capital a transparent, verifiable obligation, protected from abuse. Strategic capital planning at the outset and meticulous procedural compliance are your best investment in the legal security of your business in China. Engaging qualified local consultants (lawyers, accountants) to manage these processes is not an expense but a necessary condition for mitigating systemic risks.

Reduce Risks When Registering Your Company in China

- Choose the optimal capital contribution method

- Compliance check for foreign investors

- Registration & SAFE assistance

5 Key Questions and Answers for Foreign Investors on Rules for Contributing Registered Capital in China

According to the new revision of the PRC Company Law effective July 1, 2024, founders are obligated to fully pay up the declared registered capital within 5 years from the company’s state registration date. This rule is mandatory and aims to strengthen financial discipline. For companies registered before this date, a transition period until June 30, 2027 applies to bring their schedules into compliance with the new requirements.

Yes, such an option (non-monetary contribution) is permitted but strictly regulated. You can contribute tangible assets (equipment, real estate), intellectual property (patents, software), land use rights, or equity in other companies. The key condition: the asset must have a documented market value and be legally transferable. This requires a report from an independent, licensed Chinese appraiser. Sweat equity, business goodwill, or licenses cannot be contributed.

Illegal withdrawal of contributed capital (disguised as a loan, sham transaction, or refund) is a severe violation. Creditors or regulators may initiate “piercing the corporate veil” proceedings. In this case, founders (shareholders), as well as directors and managers who approved the transaction, bear subsidiary (personal) liability for the company’s debts with all their personal assets. The company’s limited liability is ineffective in such a situation.

Answer: Information about any changes (to the capital amount, form of contribution, payment schedule) must be disclosed by the company in the National Enterprise Credit Information Publicity System (www.gsxt.gov.cn) within 20 working days of the change. This registry is public, and its data is checked by banks, partners, and regulators. Failure to disclose on time or providing false information leads to the company being added to an “abnormal operations” list, facing fines, and having many administrative procedures blocked.

Answer: Yes, a foreign shareholder can provide the company with shareholder loans. However, their amount is limited by thin capitalization rules. There are two main regimes:

- Classical: The debt-to-equity ratio should not exceed 2:1 (for most industries).

- Based on Net Assets (NAV): The loan limit is tied to the company’s net asset value.

Important: Interest on loans exceeding the established limit is not recognized as an expense for corporate income tax purposes in China. Choosing the optimal regime requires mandatory consultation with a tax advisor. All such loans are also subject to mandatory registration with the foreign exchange authorities (SAFE).