Hongkong

Hongkong China

China

Corporate Income Tax (CIT), also referred to as Enterprise Income Tax (EIT), is the main direct tax for most companies earning income in China. The legal basis is the Law of the People’s Republic of China “On Corporate Income Tax”, which regulates in detail the procedure for determining and taxing profits.

Calculation principle and tax base

CIT is levied on the company’s net profit for the financial year, which is the difference between total revenues and allowable deductible expenses. Thus, the taxable base is adjusted gross income after taking into account all reasonable and documented costs, as well as losses carried forward from previous periods.

Key rates and benefits

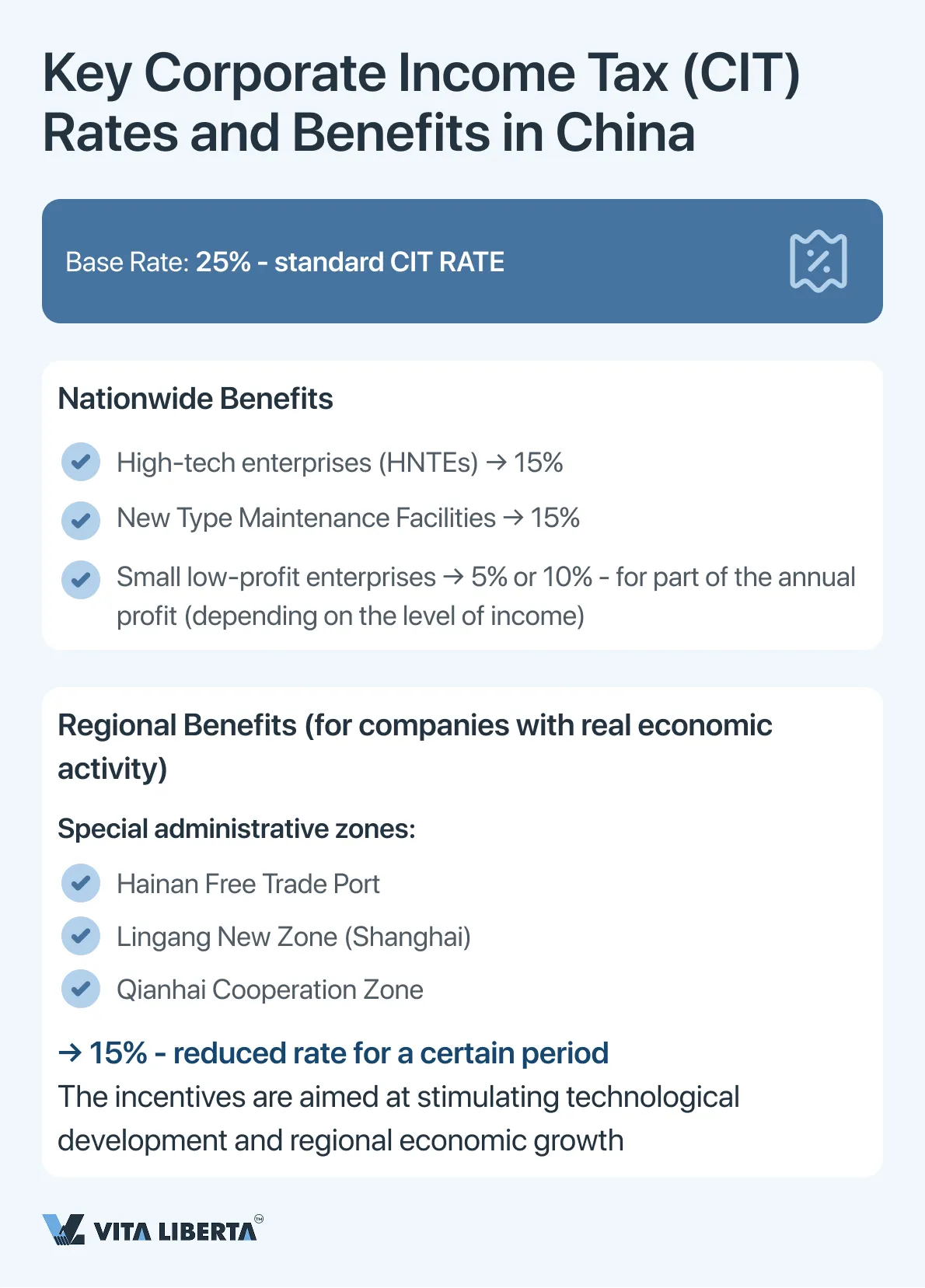

The basic (standard) CIT rate is 25%. However, the system provides for an extensive network of preferences aimed at stimulating technological development and regional growth:

- Nationwide benefits: For high-tech enterprises (HNTEs) and new type of maintenance enterprises, the rate is reduced to 15%. Small, low-profit businesses can apply an effective rate of 5% or 10% to a portion of their annual profits.

- Regional Benefits: Special Administrative Zones (e.g. Hainan Free Trade Port, Shanghai Lingang New Zone, Qianhai Cooperation Zone) offer incentive companies with real economic activity (operational substance) a rate of 15% for a certain period.

Taxpayer status and sources of income

The Chinese tax system sets its own rules of the game, and the first move in it is to accurately determine your place on the board. The key to understanding everything that follows is the answer to the question: to whom and from what? The answer forms two contrasting worlds of taxation: one for those who are inextricably linked to China’s economy, and the other for those who interact with it at a distance.

The fate of your income – global or strictly local, the ability to offset taxes paid abroad, and the very mechanism of calculation – is all predetermined by a single, but fundamental distinction: Tax Resident Enterprise (TRE) or Non-Tax Resident Enterprise (non-TRE). These are not just formal labels, but fundamentally different regimes that set the trajectory of your tax liability.

Tax Resident Enterprises (TRE) in China

This category includes enterprises registered in accordance with the legislation of the People’s Republic of China or having actual management bodies in China. TREE are subject to the principle of worldwide taxation and are required to declare all global profits received. To prevent double taxation, Chinese law provides for a mechanism for offsetting foreign taxes paid abroad on income of foreign origin. However, the amount of credit is limited to the amount of tax that would be payable in China on the same amount of income. Tax calculated at the applicable tax rates

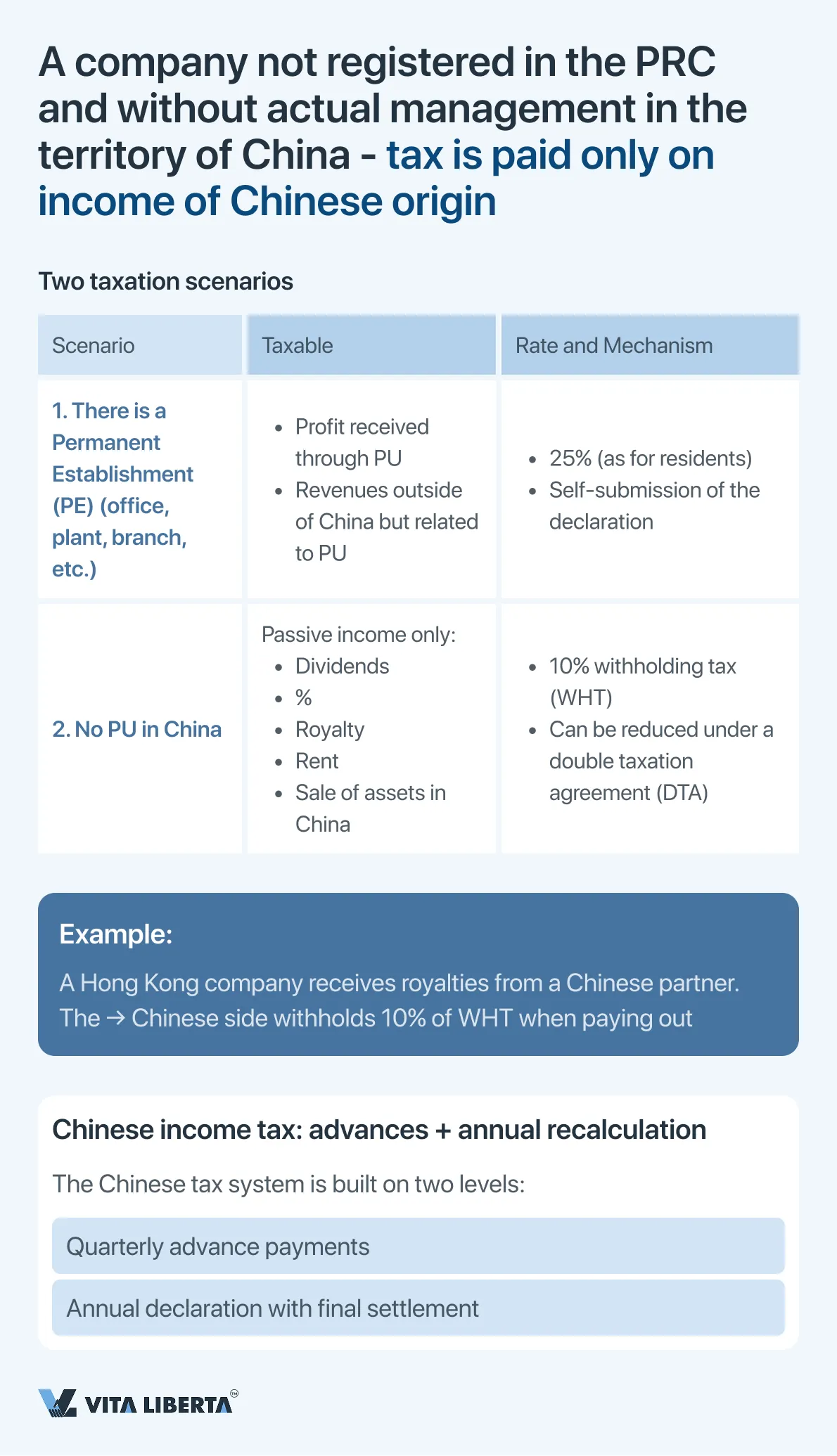

Non-Tax Resident Enterprises (non-TRE) in China

Enterprises that do not meet the residency criteria are taxed only on income of Chinese origin. In this case, a graded approach is applied:

- If there is a permanent establishment (PE) in China: The profits derived through this PE, as well as income received outside it, but effectively related to the activities of this PE, are subject to taxation.

- In the absence of a WHT: Tax is withheld at source (withholding tax, WHT) on passive income (dividends, interest, royalties, rental income, share transfer), generally at a rate of 10%, unless otherwise provided by the applicable double taxation treaty.

An important feature of the system is the impossibility of consolidating the financial results of companies belonging to the group for tax purposes. Each legal entity calculates and pays the tax independently.

China Corporate Income Tax Declaration and Payment Procedure

China’s corporate income tax (CIT) administration is based on the principle of prepayments (advances) and final annual calculation. This system ensures a uniform flow of funds to the budget and allows companies to adjust their liabilities based on actual financial results for the reporting period.

1. Advance Payments (Preliminary Declarations)

All resident enterprises (TRE), as well as non-residents (non-TRE) with a permanent establishment in China, are required to pay income tax in advance.

Frequency and timing:

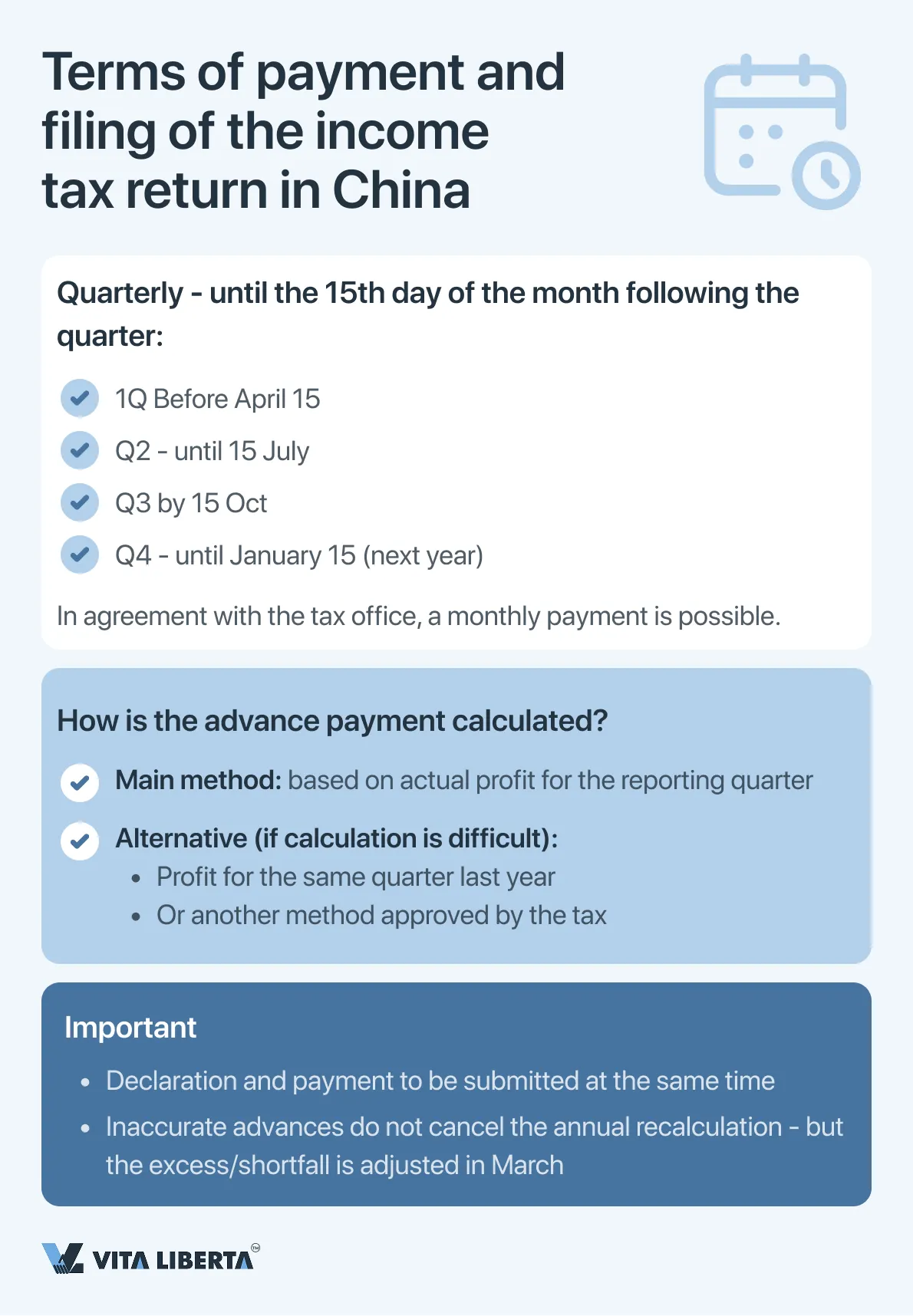

- Advance payments are made quarterly.

- The payment of the tax and the submission of the corresponding quarterly return must be made within 15 days after the end of each quarter. In some cases, in agreement with the tax authorities, payments may be made monthly.

Basis of calculation:

- As a rule, the amount of the advance payment is calculated based on the actual profit received in the reporting quarter.

- If such calculation is difficult, the tax authority may allow to use as a basis the profit for the same period of the previous year or apply another approved methodology.

2. Final Annual Declaration and Settlement

At the end of the tax year, a final reconciliation of all liabilities is carried out.

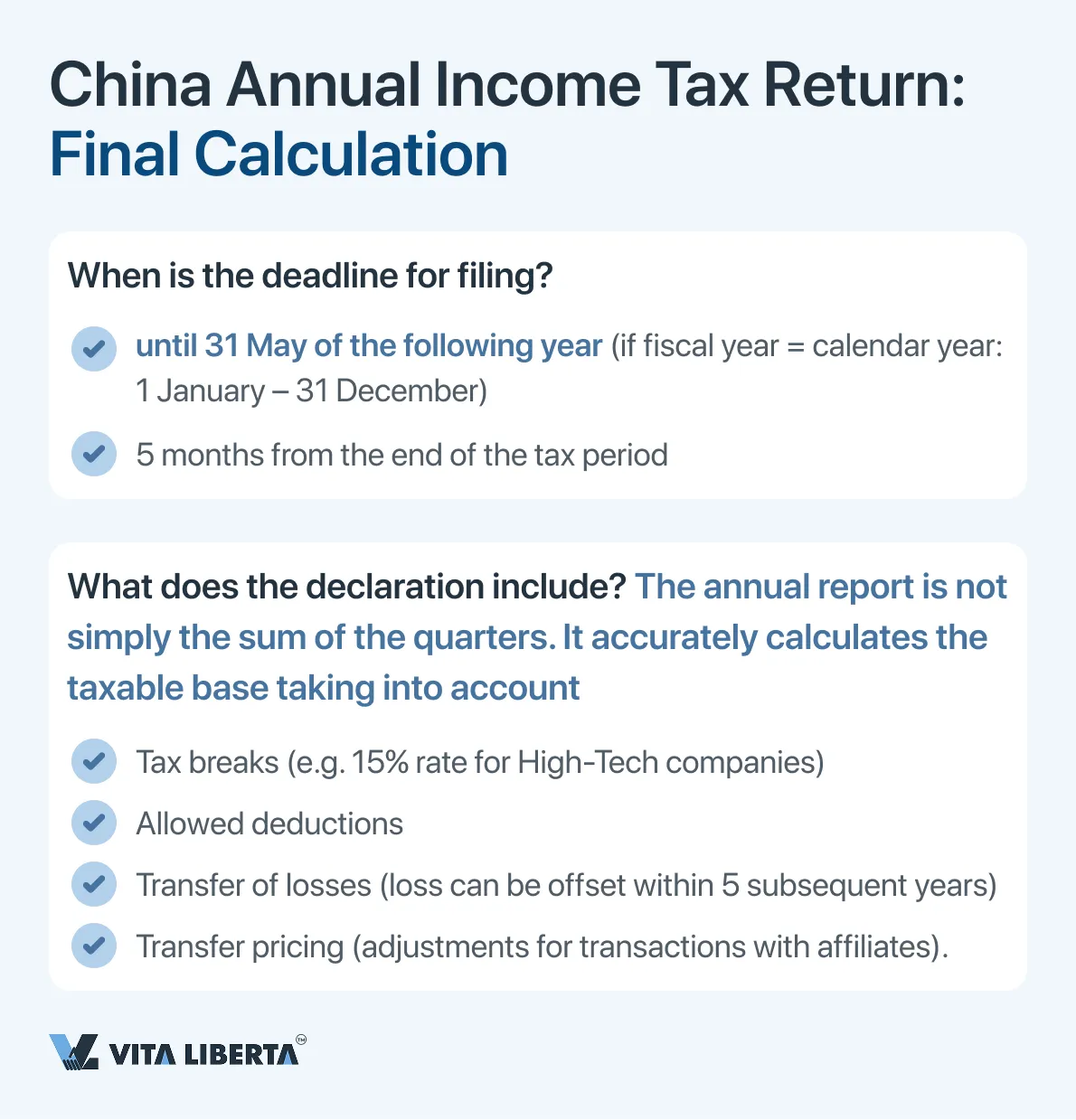

Deadline for filing: The annual CIT tax return must be filed and the final settlement made within 5 months after the end of the tax year. For most companies whose fiscal year coincides with the calendar year (ending on December 31), this period expires on May 31 of the following year.

Content of the declaration: The annual declaration serves to accurately determine the taxable base. It takes into account all statutory adjustments, such as:

- Application of tax incentives (for example, for high-tech enterprises).

- Accounting for allowed deductions (advertising, entertainment expenses within the established limits, charity expenses).

- Carry-over of losses to future periods (within 5 years).

- Transfer pricing adjustments.

Final balance: Based on the results of the annual calculation, the difference between the amount of accrued tax and the advances paid is determined. Underpayment is subject to payment to the budget with payment of late fees. Overpayment is subject to credit against future payments or refunds.

Features for different categories of taxpayers

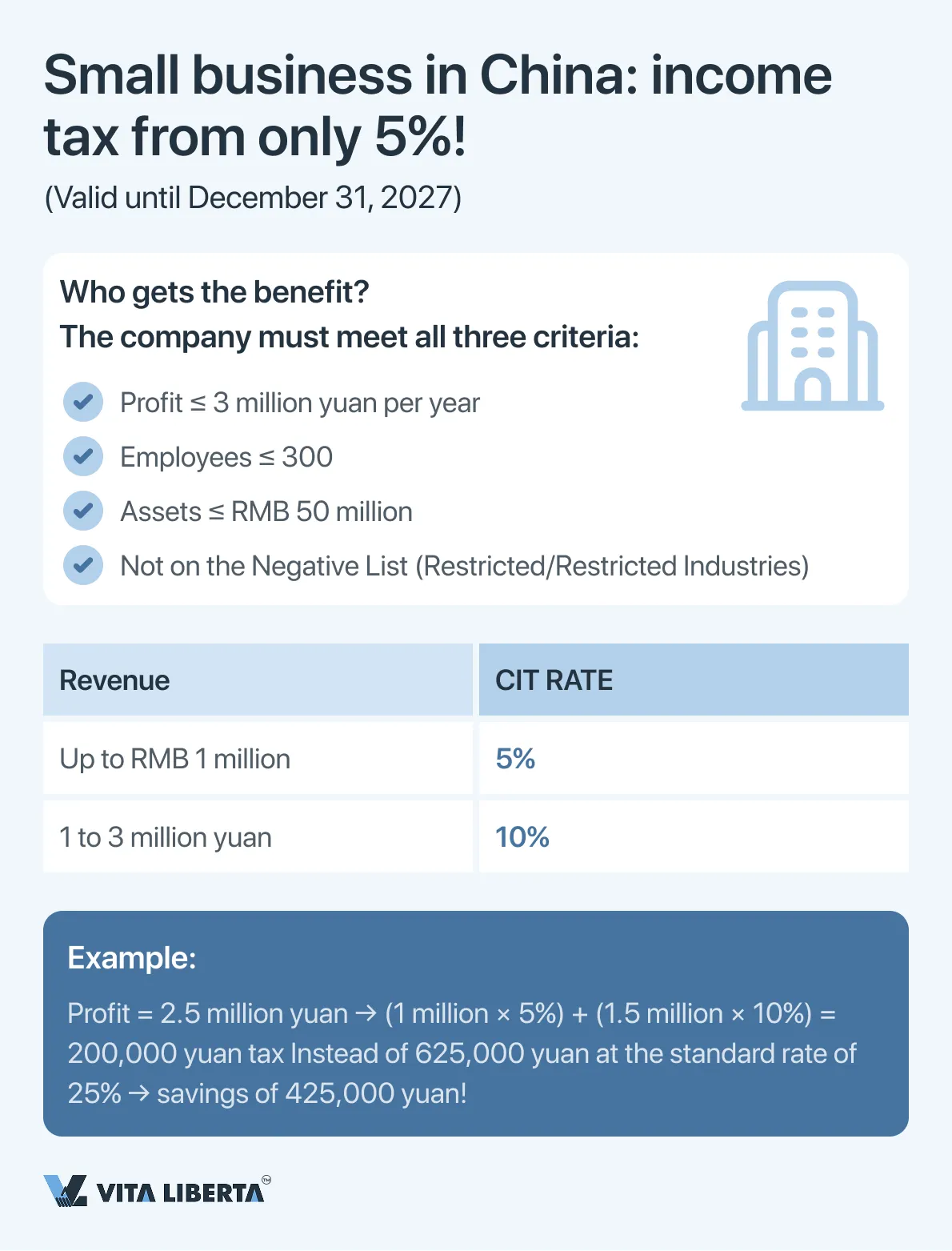

Small and marginal enterprises

For such companies that meet the criteria (annual taxable profit up to 3 million yuan, restrictions on the number of employees and assets), there are preferential effective CIT rates of 5% on part of income up to 1 million yuan and 10% on part from 1 to 3 million yuan.

The declaration procedure is similar for them, but the calculation is carried out using reducing coefficients.

Precise criteria for small and marginal enterprises

| Acceptance | Value required | Notes |

| Annual taxable profit | ≤ 3 million Chinese yuan (CNY) | Calculated for the tax year. |

| Number of employees | ≤ 300 people | |

| Total value of assets | ≤ 3 million Chinese yuan (CNY) |

The company must be registered in the PRC and engage in activities that are not on the prohibited or restricted lists.

This benefit is valid for the specified period: from January 1, 2023 to December 31, 2027.

New and High Technology Enterprises

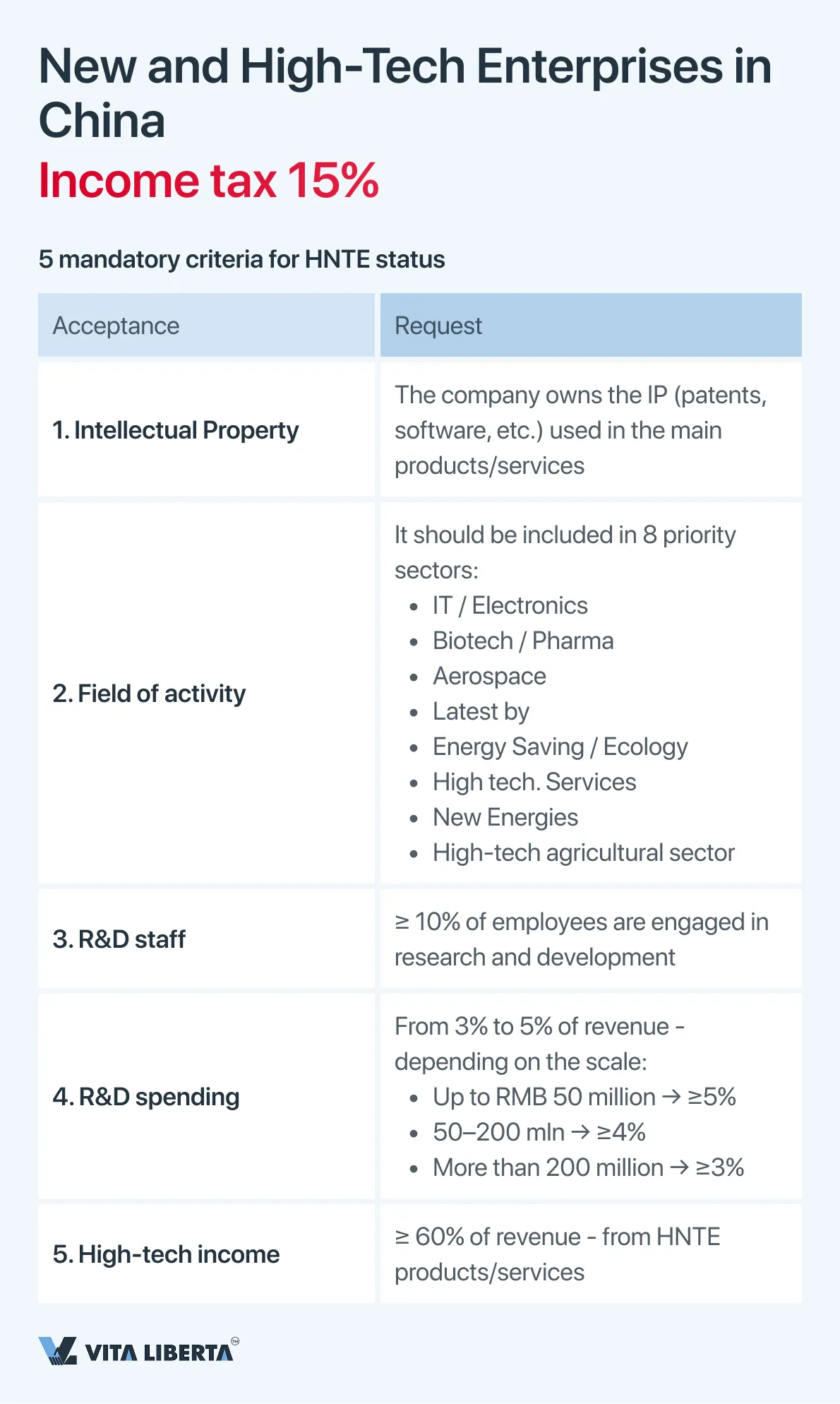

Companies that have the appropriate state certificate apply a preferential CIT rate of 15%. Confirmation of eligibility is a key element of the annual return.

In order to obtain the HNTE certificate and apply the 15% rate, the company must meet a number of strict requirements that are regularly specified by the state. The main criteria include:

- Intellectual Property Right: The Company shall own the exclusive rights to the underlying intellectual property (patents, software, etc.) used in its underlying products (services). This is a key requirement.

- Field of activity: Activities should relate to one of the 8 key areas supported by the state:

• Electronics & Information Technology

• Biotechnology and new medicine

• Aerospace

• Latest by

• High-tech service

• and Environmental Protection.

• New energy equipment

• High-tech agriculture. - The share of research and development personnel: at least 10% of the total number of employees of the company for the year should be directly involved in research and development (R&D).

- Share of R&D expenditure: The company must invest in research and development a certain percentage of revenue, which varies depending on the size of the company:

• For companies with revenue of up to 50 million yuan – at least 5%.

• For companies with revenue from 50 to 200 million yuan – at least 4%.

• For companies with revenue of more than 200 million yuan – at least 3%. - High-tech revenue share: At least 60% of the company’s total revenue must come from revenues related to its high-tech products or services.

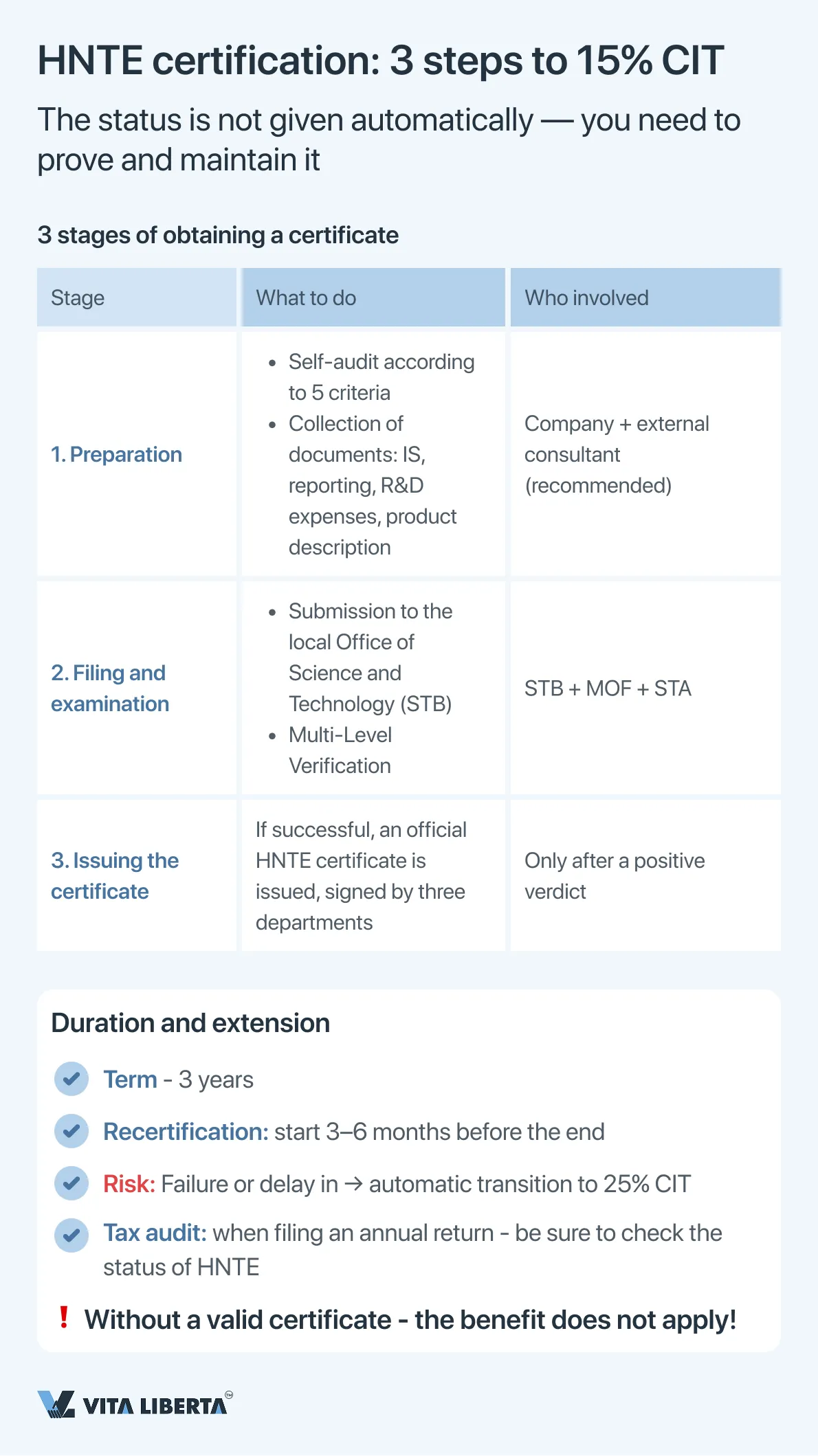

Certification and Compliance Procedure for HNTE Status

Obtaining the status of a New Type of High-Tech Enterprise (HNTE) is a strictly regulated application procedure that requires thorough preparation and interaction with government agencies. The company does not receive this status automatically on formal grounds; it is assigned based on the results of a comprehensive expert assessment.

The certification process includes the following key steps:

- Internal audit and preparation: The Company conducts a self-assessment for compliance with all 8 criteria, collects and systematizes a voluminous package of documents. This includes proof of ownership of intellectual property (patent certificates), financial statements confirming the level of R&D expenses, personnel documents, a description of the main high-tech products (services) and other materials.

- Application and examination: The prepared package of documents is submitted to the local Office of Science and Technology (STB), which acts as the main coordinator of the process. The application undergoes a multilevel examination involving specialists from the Ministry of Finance (MOF) and the State Tax Administration (STA). Experts assess both the formal compliance with the criteria and the real innovation activity of the company.

- Obtaining a certificate: in case of a positive decision of the company, an HNTE Certificate is issued, signed by the three specified departments. This certificate is the only legitimate basis for applying a preferential tax rate.

Important aspects of validity and renewal:

- INTERNATIONAL European Community legislation is applicable as explained in Chapter 2

- 3-6 months before its expiration, the company is obliged to initiate and undergo a recertification procedure (re-assessment), which is similar in complexity to the primary one. Missing deadlines or failure to recertify lead to loss of status and automatic transition to the standard CIT rate of 25%.

- Availability of a valid (not expired) certificate is a prerequisite for the application of the 15% rate when filing an annual income tax return for the relevant period. It is mandatory for the tax authorities to check the status of the enterprise at the time of filing the tax return.

Register Your Business in China with Tax Optimization

- Optimal CIT rate selection

- HNTE status & incentive support

- International business structuring

Additional Tax and Operational Benefits of HNTE

In addition to the key benefit in the form of a reduced income tax rate, the HNTE status provides access to other significant preferences:

- Super Deduction of R&D Expenditure: This is a powerful tool acting in parallel with the reduced rate. The Company has the right to increase the amount of R&D expenses recognized for tax purposes by the coefficient established by law. Current rules:

- For most HNTEs: Actual R&D costs can be deducted at 200% (i.e. an additional 100% in excess of costs incurred).

- For enterprises in the field of integrated circuits and machine-tool construction (until 31.12.2027): an increased coefficient of 220% is applied.

- This mechanism directly reduces the taxable profit before a preferential rate of 15% is applied to it, creating a cumulative effect of tax savings.

- Regional additions and simplifications: Many Special Administrative Regions and Economic Development Zones (e.g. Shanghai Lingang New Zone, Free Trade Ports) for enterprises already having HNTE status can operate:

- Additional subsidies or grants from local authorities for research activities.

- Simplified or expedited procedures for obtaining other types of permits and benefits.

- In some cases – extended lists of encouraged industries, which allows companies that do not fall under the national criteria to qualify for similar benefits at the regional level.

Thus, the status of HNTE serves not only as a tool for reducing the tax rate, but also as a strategic asset that strengthens the company’s market position, gives access to additional financing and simplifies interaction with the innovation ecosystem of China. Its maintenance requires constant attention to compliance with the criteria and timely passage of administrative procedures.

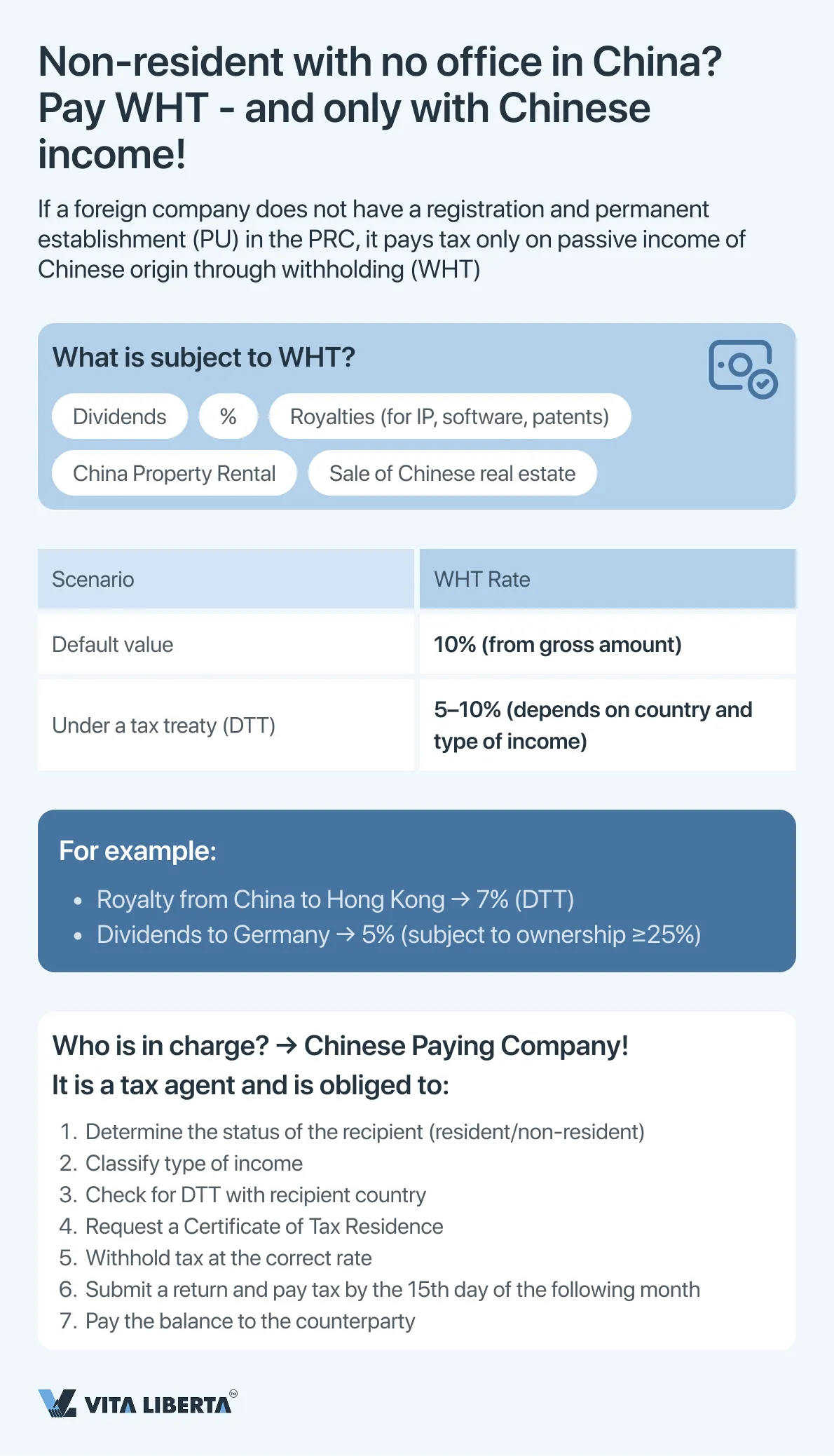

Taxation of non-residents without permanent establishment in China

For foreign companies that are not tax residents of the PRC (non-TRE) and do not have a permanent establishment (PI) in China, a special regime of taxation of income of Chinese origin is applied. The main mechanism is Withholding Tax (WHT).

Key features of the mode:

- Taxable income: The WHT regime applies to passive (non-commercial) income, in particular:

• Dividends

• %

• Royalties (payments for the use of intellectual property)

• Income from the rental of property located in China

• Income from the transfer of real estate - Base Tax Rate: The standard withholding rate is 10% of the gross disbursement amount before any taxes.

- Role and responsibility of the agent: A Chinese paying company that makes a payment to a non-resident is recognized as a tax agent (withholding agent). It bears full legal and financial responsibility for:

• Correct deduction of the calculated amount of tax from the funds payable to the non-resident.

• Timely declaration and transfer of the withheld tax to the state budget.

• Maintaining and storing primary documentation confirming the calculation and retention.

In case of non-fulfillment of obligations (incomplete retention, late payment), the tax agent is subject to fines, penalties and claims for payment of arrears at his own expense. - Agreement rate reduction: The standard rate of 10% may be reduced if a Double Tax Treaty (DTT) is in force between China and the country of residence of the foreign recipient of income. For example, the rates on many contracts for dividends are 5-10%, for royalties – 6-10%.

To apply the preferential contractual rate, the foreign recipient of income is required to provide the Chinese agent with an official Tax Residence Certificate issued by the competent authorities of their country and, as a rule, fill out a special form of the PRC tax authority.

Practical steps for a Chinese paying company:

- Recipient Status Identification: Determine whether the recipient of the payment is a PRC tax resident or not.

- Classification of income: correctly qualify the nature of the payment (dividends, interest, royalties, etc.).

- Verification of the applicable DTT: establish whether there is a valid agreement with the recipient’s country of residence and determine the rate provided for by it.

- Request for documents: request from a foreign counterparty a duly issued Certificate of Tax Residence for the application of a reduced rate.

- Calculation and withholding: calculate the amount of tax to be withheld at the applicable rate (10% or preferential contractual).

- Declaration and payment: within the established deadline (usually by the 15th day of the following month), file a WHT tax return and transfer the withheld amount to the budget.

- Payment of the net amount: transfer to a foreign counterparty the amount remaining after tax withholding.

Important: Failure to comply with the procedure may lead to reclassification of the payment and additional tax accrual at the standard rate of 10%, as well as to the accrual of penalties.

4. Income Tax Administration: E-Declaration, Timing and Responsibility

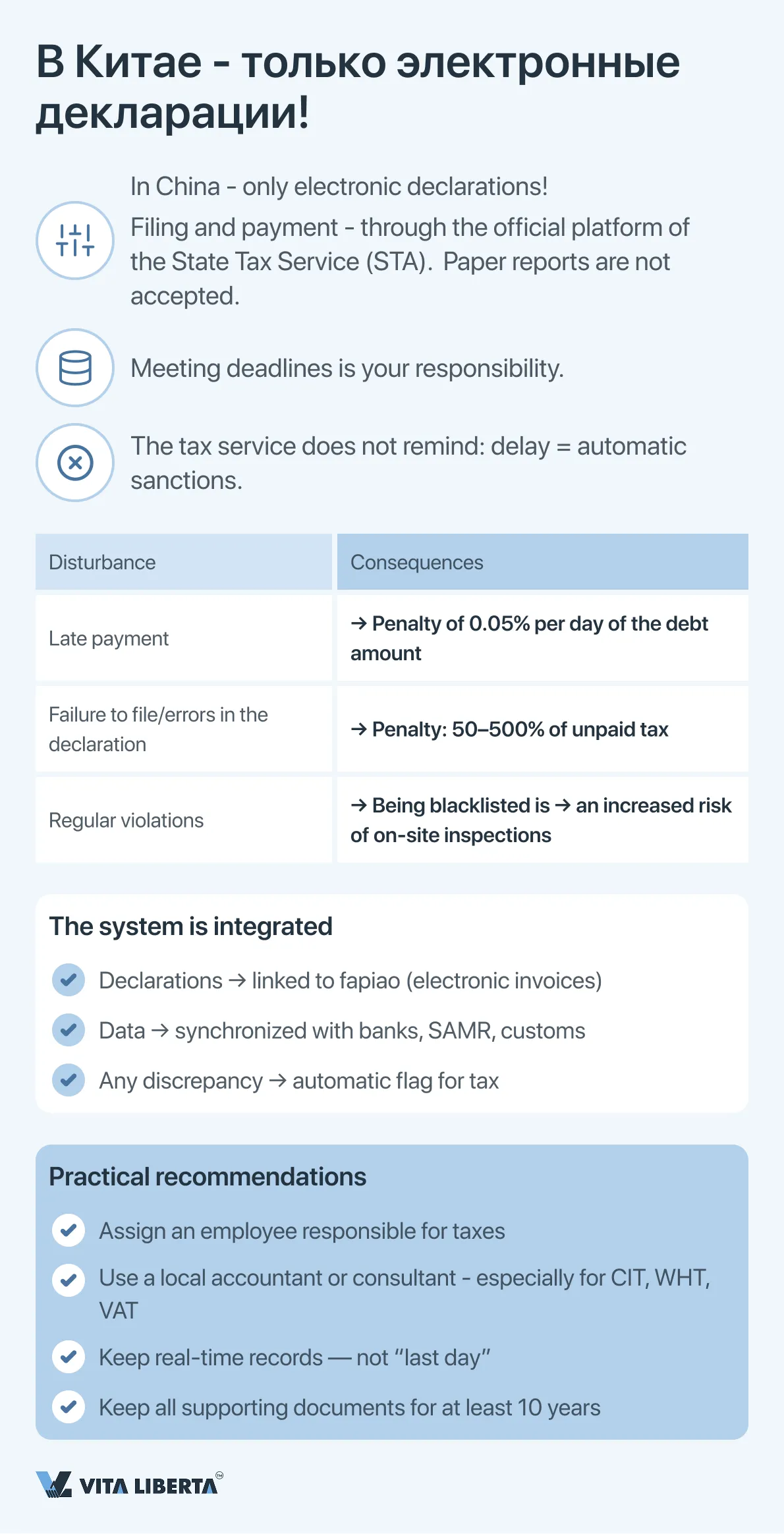

The income tax administration system (CIT) in China is fully digitalized and characterized by strict procedural deadlines, non-compliance with which entails significant financial and reputational risks.

Electronic filing and key requirements

All tax returns and reports are submitted exclusively electronically through the official online platform of the State Taxation Administration (STA). This system is integrated with electronic document management, including the system of invoices (fapiao).

The taxpayer is fully responsible for meeting the deadlines. Violation of the statutory deadlines for filing a declaration or paying tax leads to the automatic accrual of the following sanctions:

- Penalty for delay: accrued on the amount of arrears at the rate of 0.05% for each day of delay, starting from the day following the due date.

- Administrative fines: if the fact of evasion from payment is revealed, the tax authorities have the right to recover a fine in the amount of 50% to 500% of the amount of unpaid tax.

- Increased attention and audits: Companies with violations fall into the focus of increased tax supervision, which increases the risk of complex on-site inspections.

Consolidated CIT Declaration and Payment Procedure

The procedure is two-step and includes advance payments followed by an annual reconciliation.

| Stage | Deadline | Key content and documents | Remark |

| Advance payment and quarterly return | Within 15 days after the end of the reporting quarter (for most companies). Some large taxpayers may be transferred to monthly advances. | 1. Calculation of the advance payment based on the actual profit for the quarter. 2. Submission of quarterly tax return via online system STA.3. Payment of the calculated amount. | Advances paid are offset against the final annual commitment. The calculation can be made using the accrual method or the cash method (if allowed). |

| Annual Declaration and Final Settlement (Annual Reconciliation) | Within 5 months after the end of the tax year. For the year ending 31 December, the deadline is 31 May of the following year. | 1. Final calculation of the annual taxable profit, taking into account all adjustments provided for by law (for example, application of benefits, deductions, transfer of losses) .2. Submission of the Annual Declaration on CIT and a package of supporting documents.3. The audit report from a licensed Chinese audit firm is a mandatory application for a wide range of companies. | This is a key stage at which the right to preferential rates is confirmed (a valid HNTE certificate is required, etc.) and reconciliation with the advances paid is carried out. |

| Payment of the total amount or refund | Simultaneously with the filing of the annual return. | 1. Additional payment of the missing amount of tax (if advances are less than the final obligation) .2. Offsetting overpayments against future periods or processing a refund from the budget. | The return procedure can be time-consuming and requires careful justification. |

Additional requirements and best practices

- Document retention period: The taxpayer is obliged to keep all primary accounting and tax documentation, including invoices (fapiao), contracts and settlements, for at least 10 years from the end of the relevant tax period.

- Interconnection with other systems: The data submitted in the CIT declaration are checked by the tax authorities with information from other systems: VAT, payroll, customs. Any discrepancies may give rise to a request.

- Professional support: Given the complexity of the rules, especially regarding the application of benefits and deductions, as well as the high risks of non-compliance, most foreign companies engage professional tax consultants to prepare an annual return and audit documents before filing with the STA.

- Strict adherence to the schedule, accuracy of calculations and completeness of documentation are the cornerstones of impeccable tax compliance in China and allow the company not only to avoid sanctions, but also to fully exercise its rights to legitimate tax preferences.

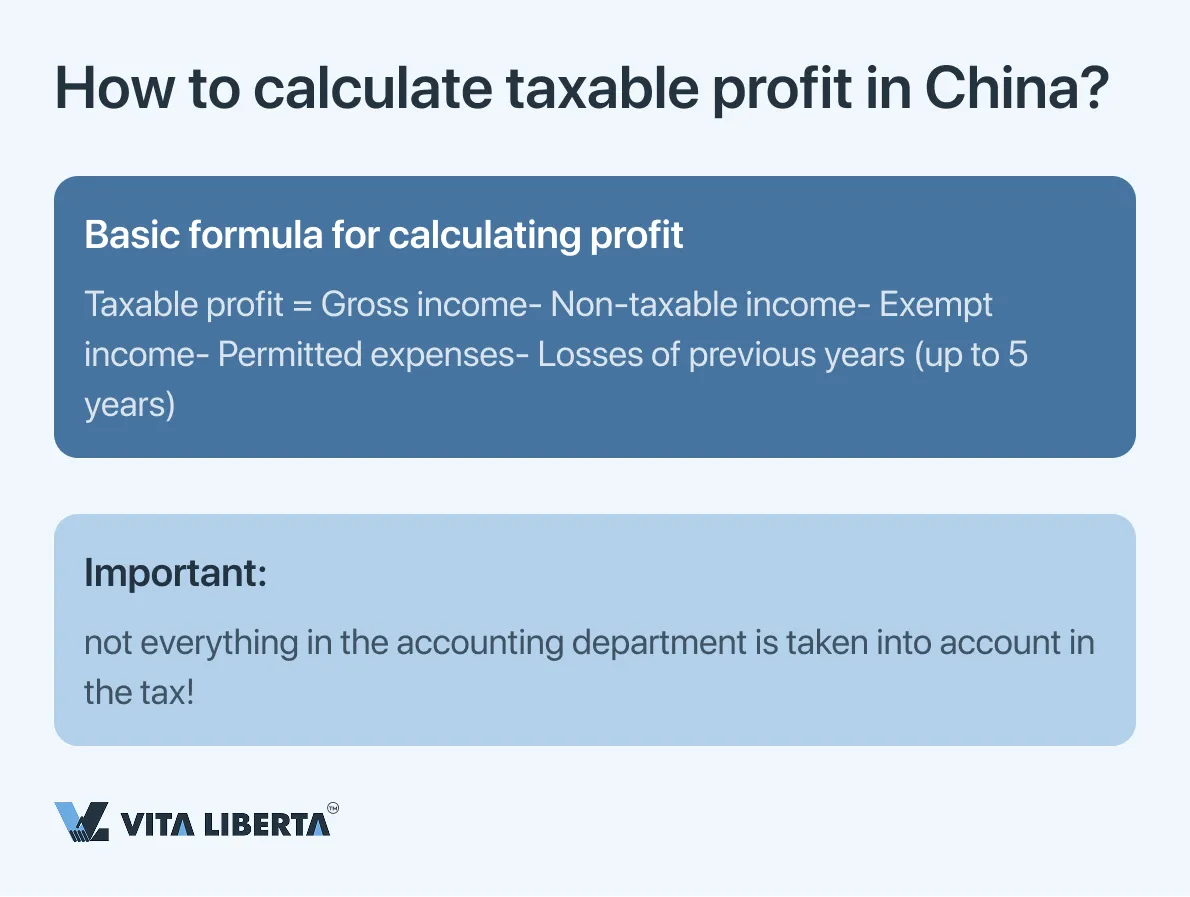

China Income Tax Base and Allowed CIT Deductions: Detailed Analysis

Determination of taxable profit is a critically important and strictly regulated process within the Chinese fiscal system. The company’s financial obligations directly depend on its accuracy, which requires an impeccable understanding and compliance with legislative norms.

Basic algorithm for calculating taxable profit

The fundamental formula for determining the tax base is fixed in the legislation and is as follows:

| Taxable profit = Total gross income – Non-taxable income – Income exempt from taxation – Allowed deductible expenses – Losses carried forward from previous tax periods |

Each element of this formula is subject to detailed rules of recognition and confirmation.

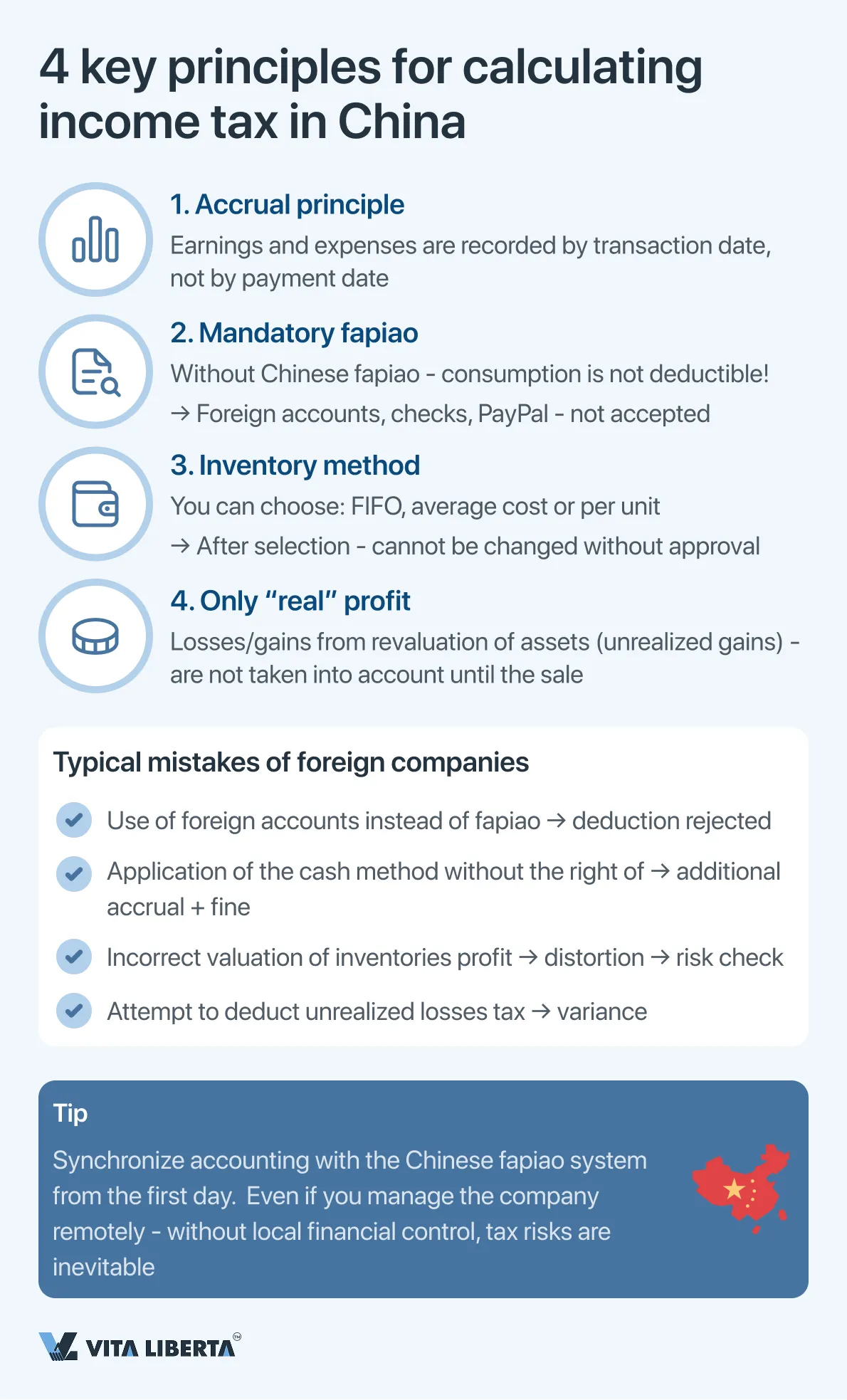

Key methodological principles and requirements

- Accrual Principle

It is a general requirement to recognize income and expenses in the reporting period to which they relate economically, regardless of the date of actual receipt or payment of funds. The cash method of accounting is allowed as an exception only for certain categories of small taxpayers, subject to the established criteria.

2. Documentary Acknowledgement Imperative (Fapiao Requirement)

Any deductible expenses to reduce the tax base must be confirmed by official Chinese tax invoices (fapiao). A properly designed fapiao is the only indisputable proof of the validity of a business transaction for the tax authorities. The absence of an appropriate fapiao makes any costs non-deductible, which is a common and costly mistake for international companies that have not adapted their financial processes to Chinese realities.

3. Inventory Valuation Methods

The taxpayer has the right to choose one of three legally allowed methods for assessing the cost of sold inventories. Subsequent arbitrary transition between methods without the consent of the tax authorities is not allowed.

- FIFO: The first units of inventory received are considered first sold.

- By weighted average cost: The calculation of the cost is based on the averages for the period.

- Specific identification method: used for unique, piecemeal or high-value assets, when it is possible to accurately track the cost of a particular unit.

4. Unrealized Gains/Losses

Gains or losses arising solely from the revaluation of assets or liabilities at fair market value (for example, on financial instruments accounted for through profit or loss – FVTPL) are not recognised for income tax purposes. Taxation of such income (or accounting for losses) occurs only at the time of their actual sale – upon sale of an asset, repayment of a liability or other completion of a transaction. This principle separates accounting from tax accounting and prevents the taxation of “paper” profits.

Features of taxation of specific types of income

| Income Type | Tax regime for CIT | Key conditions and notes (clarifications and additions) |

| Dividends between residents (TRE → TRE) | Complete freedom. | Clarified condition: Exemption applies if the recipient resident continuously owns an interest in the paying company At least 12 months This applies to any shares/stakes, not just exchange shares. |

| Dividends paid to a non-resident (TRE → non-TRE) | Withholding at source (WHT) | Base rate: 10%. Can be reduced under a Double Tax Treaty (DTT), often to 5-7% if the conditions are met (e.g. ownership share ≥ 25%). Key requirement: the entire amount of the subscribed capital must be paid before dividends are paid. |

| Foreign Income Tax Resident (TRE) | Taxable in China | 1. Foreign Tax Credit: calculated on a country-by-countrybasis. The amount of credit is limited to the amount of tax payable in China on this income.2. CFC Rules: Apply to undistributed profits of controlled foreign companies if: • Chinese residents own >10% of voting rights, and in total such ownership is ≥ 50%. • The effective CFC tax rate is below 12.5% (50% of the CIT base rate of 25%). • Important exceptions: The rules usually do not apply if the CFC is located in a country from the “white list” of the PRC (for example, the United States, Japan, the United Kingdom, etc.) or if its annual profit before tax does not exceed 5 million yuan (~$720 thousand). |

Additional clarifications and comments

- CFC rules: focus on passive income and the “essence” of transactions. Chinese CFC rules primarily target passive income (interest, royalties, dividends) accrued in low-tax jurisdictions without a reasonable commercial purpose. At the same time, in practice, tax authorities rely more on transfer pricing rules to combat base erosion than on CFC rules.

- The practical aspect of offsetting foreign tax. The offsetting procedure requires careful documentation. The taxpayer must provide Chinese tax authorities with official proof of overseas tax payment. If the foreign tax cannot be offset in the current period, it cannot be carried forward to past or future periods.

- Dividends to non-residents: compliance. A Chinese taxpayer company is obliged to fulfill the role of a tax agent: to withhold WHT, transfer it to the budget and file reports. To apply the reduced DTT rate, a foreign shareholder must submit a certificate of tax residence of his country to a Chinese company.

System of allowed deductions: Regulations and restrictions

Chinese law establishes detailed, and often limited, rules for deducting expenses.

A. Capital Expenses and Depreciation

Chinese tax law establishes detailed rules for the recognition of expenses aimed at forming a uniform tax base. Regulated depreciation methods and terms, as well as special incentive regimes, are key for capital expenditures.

The main provisions in the field of depreciation of fixed assets, enshrined in the Law of the People’s Republic of China “On Corporate Income Tax” and by-laws, are systematized in the following table:

| Aspect | Basic rules (standard mode) | Special conditions (accelerated depreciation) | Temporary incentive measures (until 31.12.2027) |

| Accrual basis | The straight-line (linear) method is the main one and is applied by default. | The application of the double-decreasing balance method is allowed for certain categories of assets. | It does not change the permissible methods, but expands the possibility of their application. |

| Minimum useful lives | Established by the Tax Rules for the implementation of the Law: • Buildings, structures: 20 years. • Equipment, transport, production equipment: 10 years. • Vehicles (except railway, water, air): 4 years. • Electronic equipment: 3 years. | The period may be reduced, but may not be less than 60% of the minimum period established in the basic rules. | For new equipment of manufacturing industries and enterprises engaged in R&D, it is allowed to reduce the depreciation period to 60% of the minimum. |

| Application conditions | Applies to all depreciable assets. | Permitted for equipment that: 1. It is subject to strong obsolescence due to technologicalprogress.2. Constantly works in conditions of increased vibration, severe corrosion or other corrosive environments. | 1. One-time write-off for expenses: for new equipment and tools (except buildings) at a cost of no more than 5 million yuan per unit. Available to businesses in all industries.2. Accelerated depreciation: for new equipment worth more than 5 million yuan (method and term – at the choice of the enterprise within the permitted limits) .3. Special regime for manufacturing industries and R&D: the right to write off new equipment at a time, regardless of its cost. |

| II. The procedural aspect | Does not require additional approvals. | For the application of accelerated depreciation on common grounds (paragraph 2), prior approval (registration) of the method with the tax authority is required before its use. | No special permission of the tax authority is required for the application of temporary incentive measures. The enterprise independently chooses the method when registering the asset, but must be ready to confirm the compliance of the asset with the criteria (new, for production purposes, etc.). |

KEY FINDINGS AND RECOMMENDATIONS

- Two accelerated depreciation modes. It is important to distinguish between a permanent special regime (for specific equipment) and a temporary stimulating regime (valid until the end of 2027). The latter, especially the one-time write-off rule, is a powerful tool for tax optimization and cash-flow improvement.

- Critical importance of documentation. Regardless of the chosen method, the company is obliged to keep a complete and correct record of fixed assets, confirm their initial cost and technical characteristics. For accelerated depreciation on common grounds, a package of coordination documentation with the tax authority is mandatory.

- Strategic investment planning. Until 2027, enterprises, especially in the manufacturing and scientific and technical industries, should make maximum use of the possibility of a one-time write-off of the cost of new equipment to reduce the tax base of the current period.

B. Incentive deductions for R&D

Super Deduction of research and development (R&D) costs is one of China’s most powerful tax instruments to stimulate innovation. It allows to significantly reduce the taxable profit by multiplying the actual costs.

- As a general rule, actual R&D costs incurred that are not capitalized into intangible assets may be deducted at a rate of 200% of their amount.

- Increased coefficient: for enterprises in the field of integrated circuit production and machine-tool construction in the period 2023-2027, the coefficient is 220%.

- Capitalized expenses: if R&D expenses have formed an intangible asset, its carrying amount for depreciation purposes can be increased by the same percentage (200% or 220%).

Incentive deductions for R&D

| Aspect | Data | Clarified and supplemented information |

| Total coefficient for current expenses | 200% of the amount of expenses (coefficient 2.0). | Confirmed. Actual R&D costs incurred and recorded as expenses of the current period are deducted from the tax base in the amount of 200% of their amount (coefficient 2.0). |

| Increased ratio for priority industries | 220% for the production of integrated circuits and machine tools (2023-2027). | To be confirmed and clarified. The coefficient of 220% (2.2) is set for enterprises in priority areas, such as the development of integrated circuits and industrial robotics, and is valid at least until the end of 2027. |

| Coefficient for capitalized expenses | The book value of intangible assets increases by 200% or 220%. | Requires adjustment. If R&D expenses are capitalized and formed an intangible asset, its depreciation base increases to 320% (coefficient 3.2) of the original cost, regardless of what coefficient (2.0 or 2.2) current expenses would be written off. |

Key aspects for practical application

- Combination of benefits (Cumulative Benefit): Companies with the status of a high-tech enterprise (HNTE) are entitled to simultaneous application of:

- Reduced CIT rate of 15%.

- Super deduction of R&D expenses (200% or 220%).

This creates a synergistic effect, making the effective tax burden for innovative companies one of the lowest in the world.

2. Definition and documentation of expenses: The deduction does not apply to all expenses, but only to those directly related to R&D activities and falling under the established categories:

- Salaries of researchers.

- The cost of raw materials and materials for experiments.

- Depreciation of equipment used exclusively in R&D.

- The cost of third-party R&D services (with restrictions).

- Other Direct Costs (ODCs):

A mandatory requirement is to maintain a separate detailed accounting (auxiliary accounting) of such expenses and the availability of a complete package of primary documents.

3. Procedural requirements and audit:

- No prior authorization from the tax authorities is required to apply the deduction.

- The company independently declares the right to deduction by filling out the relevant sections of the annual tax return.

- All R&D expenditure documentation must be kept and ready for submission during a desk or on-site tax audit. The tax authorities pay special attention to the validity of attributing costs to R&D.

Strategic recommendation: To maximize benefits, companies need to implement internal procedures to accurately identify, account for and document all R&D-related costs. This will ensure the indisputable application of the super deduction and will allow to take full advantage of China’s innovative tax policy.

B. Deduction of Finance Costs: The Thin Capitalization Rule

Thin capitalization rules control the deduction of interest on loans to prevent artificial replacement of equity with debt financing in order to erode the tax base. These rules apply primarily to debt owed to related parties.

Safe debt load (coefficient):

- For non-financial enterprises: 2:1 (debt to equity ratio).

- For financial institutions: 5:1.

Interest accrued on loans from related parties exceeding the limit calculated at the specified ratios is not deductible in the current period, but can be carried forward.

Principles of application of thin capitalization rules:

| Aspect | Principe | Clarifications and practical aspects |

| The essence of the rule | Limiting the deduction of interest on controlled debt to prevent tax erosion. | The rule is aimed at transactions between related parties. Interest on loans from independent banks or financial institutions is generally not subject to these restrictions if the arm’s length principle is observed. |

| Safe ratio (debt/equity) | • 2:1 for non-financial businesses • 5:1 for financial institutions | The ratio is calculated as the ratio of controlled debt (to related non-resident parties) to the borrower’s equity. Equity for calculation purposes is usually determined on the basis of accounting data. |

| Consequences of exceeding the limit | Interest calculated on the amount of excess of the safe ratio is not deductible in the current tax period. | • Carry-over: Non-refundable interest can be carried forward and deducted in subsequent tax periods, but for no more than 5 years. • Calculation: Deduction Limit = (Total Controlled Debt Interest Amount) × (Safety Ratio / Actual Debt Ratio). |

| Key Exclusions (Grounds for Total Deduction) | Even if the safety factor is exceeded, interest can be deducted completely if certain conditions are met. | 1. Arm’s Length Principle: The Company may prepare and provide, at the request of the tax authorities, a Thin Capitalization Special Issue File proving that the terms of the loan comply with marketconditions.2. Lender with a higher tax rate: If the loan is provided by a related party resident in the PRC, whose actual effective income tax rate is higher than that of the borrowing company. |

D. Limited and regulated operating expenses

| Cost Category | Deduction limit | Key Terms |

| Charitable donations | ≤ 12% of annual profit before tax | The above-limit part can be postponed for the next 3 years. Donations to targeted poverty alleviation projects (2019-2025) are fully deductible (100%). |

| Advertising and promotional expenses | ≤ 15% of annual sales revenue (for cosmetics, pharmaceuticals, beverages – ≤ 30%) | The above-limit portion can be carried over for an unlimited number of future periods. Complete ban on deductions for the tobacco industry. |

| Entertainment expenses | ≤ 60% of actual costs incurred OR ≤ 0.5% of annual revenue (whichever is lower) | The above-limit part is not subject to postponement to future periods. |

| Business travel expenses | Strictly within the standards established by the Ministry of Finance and THE State Tax Service for different regions and levels of employees. | Primary documents (tickets, hotel invoices) are required. Expenses in excess of the norms are not deducted. |

E. Carry-over of prior years’ losses in China: detailed rules and administrative requirements

China’s loss carry-forward policy is a highly regulated instrument that, while providing businesses with the ability to offset future profits, comes with significant constraints and procedural complexities.

Carry forward: Allowed for up to 5 years for most businesses.

Extended period: for high-tech enterprises (HNTEs) and small technology companies, the transfer period is increased to 10 years.

Carry-over: Not allowed under any circumstances.

This deduction system, which combines stringent regulations with incentive overdeductions, requires companies to carefully plan their taxes and document all transactions flawlessly. Compliance with limits and conditions is the subject of close attention of tax auditors

| Aspect | General regulation | Clarifications, exceptions and administrative requirements |

| Standard rescheduling period | 5 years from the year following the year of occurrence of the loss. | Confirmed by Article 18 of the Law “On Corporate Income Tax”. Compensation is carried out in chronological order: the earliest losses are first offset. |

| Extended term (10 years) | For high-tech enterprises (HNTE) and small technology companies. | Strict clarification required: Not all HNTEs are eligible for a 10-year rollover, but a narrower category, the National Tech SME.Tech SME Key Criteria: • Annual revenue ≤ 200 million yuan (~$28 million). • Number of employees ≤ 300 • The book value of assets is ≤ 400 million yuan. |

| Prohibition on backward transfer | Completely prohibited. | Chinese tax law does not provide for a carry-back loss mechanism. It is not possible to refund or offset the previously paid tax against the losses of the current period. |

| Fundamental constraint | Lack of tax consolidation at the group level. | Losses can only compensate for future profits of the same legal entity in which they were incurred. Consolidation of financial results within the group of companies is not allowed. |

| Quantitative limit and accounting | There is an annual limit on the amount of credit. | Detail: 1. Limit of Indemnity: The amount of loss credited in a particular year may not exceed 70% of that year’s taxable profit before deducting the loss. The remaining 30% of profits are taxed in full.2. Mandatory separate accounting: The Company is obliged to maintain and keep a detailed tax register of losses carried forward, broken down by years of occurrence, amounts and history of use. |

Critical Conclusions and Practical Recommendations

- Careful verification of eligibility for extended term: Companies with HNTE status should not automatically rely on a 10-year carry-over period. It is necessary to conduct a separate analysis of compliance with the more stringent National Tech SME criteria. Misuse of the 10-year term is a common reason for additional tax charges and fines during audits.

- Strategic planning with 70% limit: The 70% rule means that even if there are significant carry-over losses, the company will pay CIT annually on at least 30% of its current profits. This factor must be taken into account in financial modeling, investment project evaluation and cash flow management.

- Administrative discipline as the basis of protection: in the conditions of close attention of the tax authorities to the mechanisms of transferring losses, the presence of properly organized, transparent and easily audited internal tax accounting is not a recommendation, but a prerequisite. The absence of such accounting or its non-compliance with the standards may lead to a complete refusal to recognize losses of previous years and significant financial losses.

Thus, the loss carry-over system in China, for all its potential utility, is a complex administrative tool that requires a deep understanding of regulatory intricacies, meticulous documentation, and an integrated approach to tax planning.

China Income Tax: Strategic Insights for Effective Tax Planning

The profit tax system in China is a complex but structured mechanism that seamlessly combines the fiscal function with industrial and regional policy instruments. Its effective use requires companies not to passively follow the rules, but to take an active strategic approach.

The key paradox of the system is the simultaneous operation of two principles: strict formalization (fapiao imperative, deduction limits, detailed procedures) and flexible incentive support (R&D excess deductions, accelerated depreciation, preferential rates). Success is determined by the ability of the company not only to comply with the first, but also to maximize the implementation of the second.

Strategic imperatives for different categories of taxpayers:

- For innovative companies: The central element should be a dual strategy – obtaining the status of High and New Tech Enterprise (HNTE) for a rate of 15% and parallel maximization of the super deduction of R&D costs (200%/220%). Investments in the relevant document flow and internal accounting are paid off by a multiple reduction in the effective tax burden.

- For enterprises with foreign participation: it is critically important to correctly determine tax residency and the presence of a permanent establishment, which fundamentally affects the amount of liabilities. The structuring of intra-group transactions (loans, royalty payments) requires advance consideration of thin capitalization and transfer pricing rules to protect interest deductions.

- For all companies: Procedural discipline is a universal requirement. Keeping the deadlines for electronic filing, keeping separate records for preferential deductions (R&D, charity), forming a dossier to confirm the right to benefits (for example, for HNTE status or the application of a reduced WHT rate under the contract) is not a formality, but the basis for reducing risks and exercising tax rights.

The general trend of China’s tax policy is obvious: stimulating the transition to an innovative, high-tech and “green” economy. Tax incentives are purposefully concentrated in the areas of R&D, integrated circuit manufacturing, machine tool building, environmental protection, as well as in priority development regions.

Thus, income tax in China should be considered not only as a mandatory payment, but also as a tool for strategic management of business value. A deep understanding of the system, proactive planning of operations and impeccable compliance make it possible to transform potential fiscal obligations into a competitive advantage, ensuring sustainable growth in one of the most dynamic economies in the world.

Reduce Your Tax Burden & Risks in China

- Corporate Income Tax (CIT) audit

- WHT & Double Tax Treaty (DTT) review

- Error-free reporting preparation

China Corporate Income Tax (CIT) FAQ

This fundamental difference determines the entire treatment of your taxation.

Tax Resident Enterprise (TRE): This category includes companies registered under the laws of the People’s Republic of China, or those whose actual management is located in China. TRE are subject to the principle of worldwide taxation. This means that they are required to declare and pay tax in China on all their profits earned both domestically and abroad. To avoid double taxation with foreign income, a credit for taxes paid abroad (with restrictions) is applied.

Non-Tax Resident Enterprise (non-TRE): These are companies that are not registered in China and are managed from abroad. They are taxed only on income of Chinese origin. If a non-TRE has a permanent establishment (office, factory) in China, it pays tax on the profits of that establishment. If there is no permanent establishment, then passive income (dividends, royalties, interest) is subject to withholding tax (usually 10%).

An error in determining status can lead to serious tax surcharges, fines, and penalties. For example, if a non-TRE conducts an activity that the tax authorities recognize as a permanent establishment, all profits from that activity may become taxable in China at the full rate.

It is a powerful tool to support small businesses until the end of 2027. Reduced effective rates are applied instead of the standard rate of 25%.

Benefit Criteria: The Company must meet all of the following conditions at the same time:

- Profit: Annual taxable profit does not exceed 3 million yuan.

- Personnel: The average number of employees is not more than 300 people.

- Assets: The total value of assets does not exceed 50 million yuan.

The company should not engage in business activities from prohibited or restricted by the state lists.

Calculation mechanism: The tax is calculated on a progressive scale:

- A 5% rate is applied on a part of the annual profit up to 1 million yuan.

- A 10% rate is applied on part of the profit from 1 to 3 million yuan.

Example: if the profit is 2.5 million yuan, the tax will be (1,000,000 * 5%) + (1,500,000 * 10%) = 200,000 yuan. At the standard rate of 25%, the tax would be 625,000 yuan. The savings are 425,000 yuan.

The status of HNTE is an official confirmation that the company is innovative, and the key to reducing the income tax rate to 15%, as well as to other preferences.

The company must meet a number of strict criteria, including ownership of key intellectual property, working in a priority high-tech industry, having a certain share of employees in R&D (≥10%), the level of R&D spending on revenue (from 3% to 5%) and the share of high-tech income (≥60%).

This is not an automatic procedure. The company must prepare a voluminous package of documents, undergo an internal audit and apply to the local Office of Science and Technology. The application undergoes a multi-level examination with the participation of the tax authorities and the Ministry of Finance.

The HNTE certificate is valid for 3 years only. 3-6 months before the expiration date, the company is obliged to undergo a recertification procedure similar to the primary one. Failure or delay leads to the loss of status and the transition to a rate of 25%. The tax authorities must check the availability of a valid certificate when accepting the annual return.

The Chinese tax system is built on the principle of strict documentary evidence.

Any deductible expenses to reduce the tax base must be confirmed by official Chinese tax invoices (fapiao). Checks, foreign invoices, PayPal payments, etc. are not accepted by the tax authorities as a basis for deduction. The absence of a correct fapiao makes expenses non-deductible.

Limited deductions: Even with fapiao, many categories of operating expenses have statutory limits:

- Charity: no more than 12% of annual profit.

- Advertising expenses: no more than 15% of revenue (for some industries — 30%).

- Entertainment expenses: are deductible only up to 60% of the actual amount or 0.5% of the revenue (a lower limit applies).

Tax planning in China should begin with setting up internal financial processes to require fapiao for all transactions and taking into account industry spending limits.

The system is based on advance payments followed by annual reconciliation and is fully digitalized.

Quarterly advance payments and declarations:

- Deadline: you must pay the tax and submit the e-declaration within 15 days after the end of each quarter (for example, for the 1st quarter – before April 15).

- Basis: Calculation, as a rule, is carried out from the actual profit for the quarter.

Final annual declaration and calculation

- Deadline: The return must be filed and the final settlement made within 5 months after the end of the fiscal year. For the year ending 31 December, the deadline is 31 May of the following year.

- Table of contents: This is the key stage at which the final tax base is determined, taking into account all benefits (for example, by HNTE status), deductions (including R&D super deduction), loss carry-over (up to 5 years) and adjustments. The declaration is often required to be accompanied by an audit report from a licensed Chinese firm.

A reconciliation is made with the advances paid. Any shortfall is paid with penalties, overpayment is credited or refunded.

All actions are performed through the online platform of the State Tax Administration (STA). The delay entails the automatic accrual of penalties (0.05% per day) and the risk of fines.