Hongkong

Hongkong China

China

The same product can jump 13% in price over two lines on a customs form. Here is how Chinese VAT actually works — and where a business loses money or wins it back.

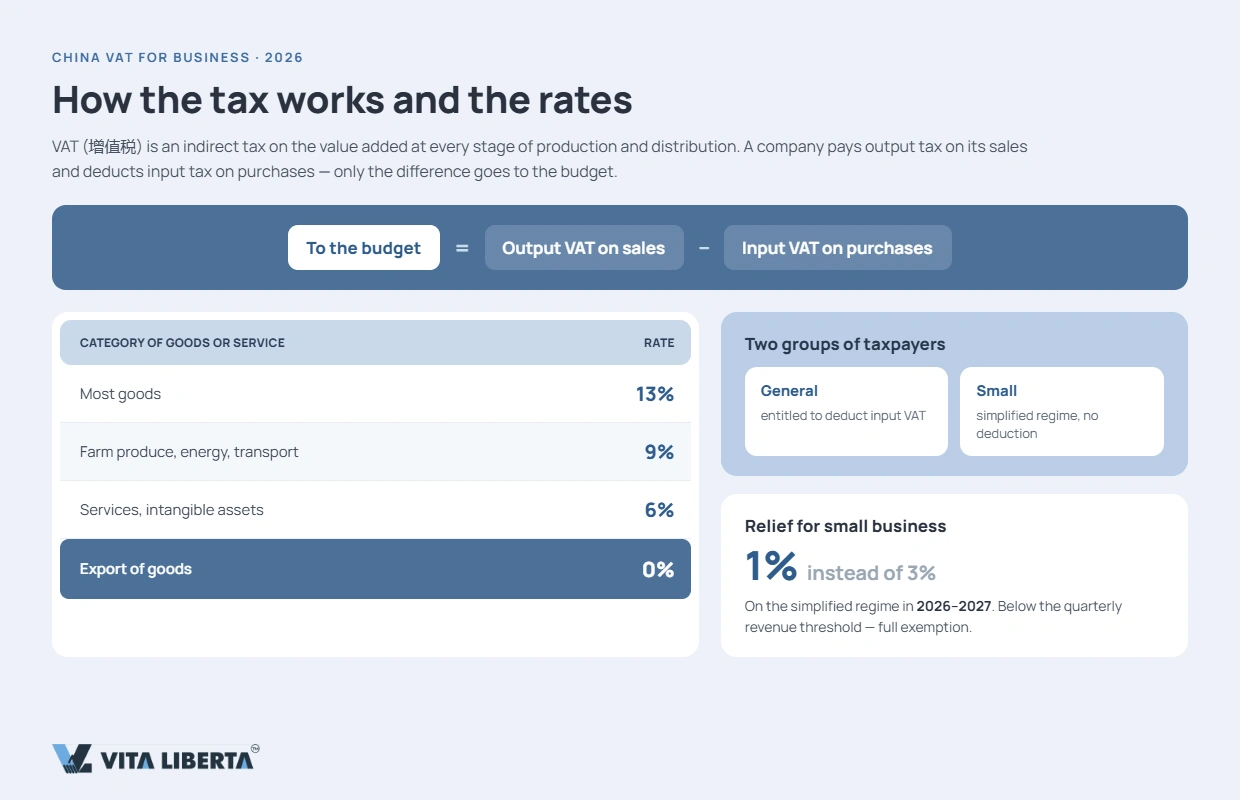

How the tax works

VAT in China (增值税, zēngzhíshuì) is an indirect tax charged on the value added at each stage of production and distribution. A company pays output VAT on its sales and offsets the input VAT paid on its purchases; only the difference goes to the state. Payers fall into two groups: general taxpayers, who can claim input credits, and small-scale taxpayers, who sit under a simplified regime.

The rate bands

| Category | Rate |

| Most goods | 13% |

| Agricultural products, energy/utilities, transport | 9% |

| Services, intangible assets | 6% |

| Export of goods | 0% |

Relief for small businesses

Small-scale taxpayers under the simplified system pay 1% instead of 3% across 2026–2027, and can be exempt entirely where turnover stays below the quarterly threshold. Software development and consulting, for example, fall into the 6% services band.

Lost in China’s VAT rates?

- Right rates for your business

- Check your VAT refund eligibility

- Taxpayer status factored in

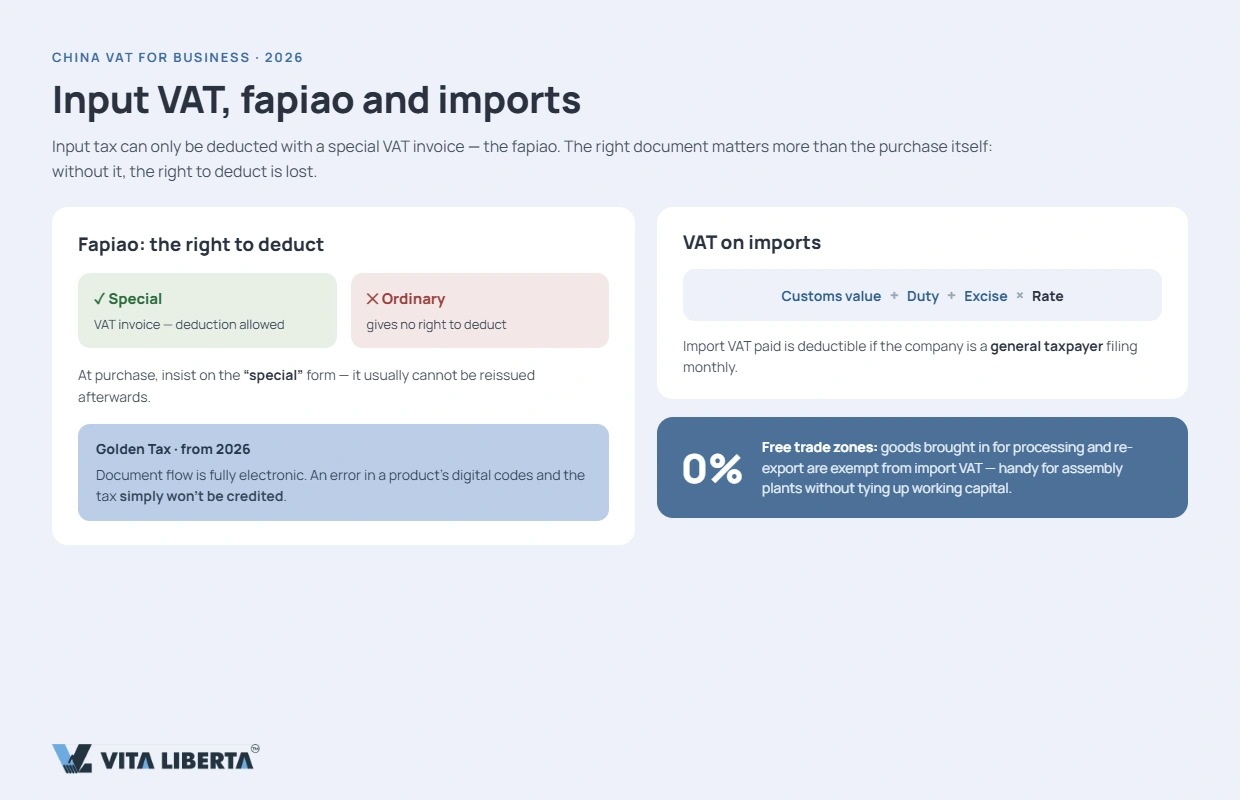

Input VAT and the fapiao

Input VAT is deductible only against a special VAT fapiao. An ordinary invoice carries no right to credit, so at the point of purchase you insist on the “special” form. From 2026 the whole invoice trail is electronic and tied into the Golden Tax System: one wrong digital product code and the tax simply won’t be credited.

Import VAT

Import VAT is calculated as (customs value + duty + consumption tax) × rate. The amount paid is creditable if the company holds general-taxpayer status and files monthly. One structural advantage: goods brought into a free trade zone for processing and re-export carry no import VAT — useful for assembly operations that don’t want working capital frozen.

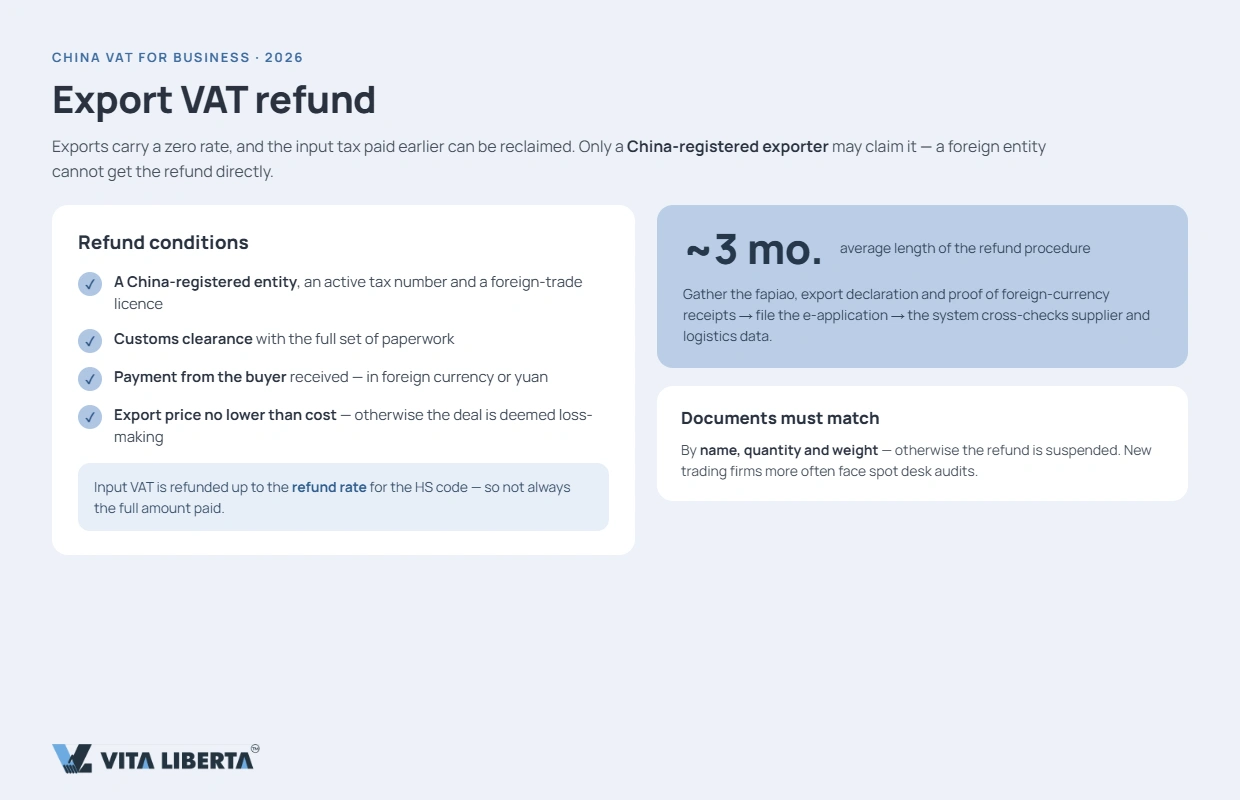

Reclaiming export VAT

Exports are zero-rated, and the input VAT already paid can be recovered.

Who qualifies, and on what terms

Only an exporter registered in China can claim. What that requires:

- a China-domiciled legal entity, an active tax number and a foreign trade licence;

- goods cleared through customs with the full documentary set;

- payment received from the overseas buyer — in foreign currency or in RMB;

- an export price no lower than the purchase price (otherwise the deal reads as loss-making).

Input VAT comes back only up to the refund rate set for that product by HS code — not always the full amount paid. A foreign legal entity cannot receive the refund directly; a Chinese company is the mechanism.

Process and timing

The procedure takes roughly three months. You assemble the fapiao, the export declaration and confirmation of the foreign-exchange settlement, file electronically, and the system reconciles the data against supplier and logistics records. Every document must agree on description, quantity and weight, or the refund is suspended. Newly formed trading firms are the ones most often pulled for desk audits.

What changed in 2026

From the start of 2026 the new VAT Law took effect: the rates themselves are unchanged, but enforcement and digital administration are tougher. Then from 1 April the rebate was cut across a set of export categories — solar panels and modules lost it in full, while batteries dropped from 9% to 6% for the remainder of 2026, to be removed entirely from 2027.

⚠️ The point that catches people: the refund rate that applies is fixed by the export date on the customs declaration — not the day the contract was signed or the money moved. A batch that left the country on 2 April under a January agreement no longer qualifies for the old rate.

Sellers push the lost rebate into the price, so for these categories the cost to an overseas buyer has risen by roughly 9–13%.

VAT on services bought from abroad

When a Chinese company buys services from an overseas provider — consulting, IT, engineering — consumed inside China, the Chinese buyer must withhold the tax as a withholding agent. If the foreign supplier has a registered establishment in the PRC, that entity handles assessment and payment instead. For an overseas software vendor or consultant selling to a Chinese client, this is material: the tax is effectively deducted at the customer’s end.

Risks and common failures

- the supplier books the deal as a domestic sale instead of an export and keeps the tax — up to 13% gone;

- shipping around the Chinese declaration via Hong Kong, Vietnam or the UAE yields no refund;

- a name mismatch between fapiao and declaration freezes the claim;

- firms with a foreign beneficial owner draw more questions — documents, statements, proof of address.

“Reclaiming VAT in China is about documentary discipline, not luck. Most rejections grow out of paperwork mismatches or a faulty fapiao, not from an inspector nitpicking. Get the documents right first; the export is secondary.”

— Sergey Konon, China tax consultant

Chinese VAT comes down to the 13/9/6/0% bands and a refund mechanism that in 2026 turned stricter and fully digital. A foreign business is better off operating through a Chinese entity, keeping its special fapiao in order and watching the export date. Check the refund rate for your product first, then build the shipment — that way the tax never turns into a hidden loss.

Note for Hong Kong readers: Hong Kong is a separate tax jurisdiction with no VAT or GST at all, and mainland VAT rules do not extend to Hong Kong or Macau. Treat any mainland fapiao you receive as a document to verify on the STA’s national platform, not to take at face value.

Need help with China VAT?

- VAT taxpayer registration

- Export VAT refunds

- Ongoing reporting support

FAQ

The baseline is 13% for most goods; 9% covers agricultural products, transport and construction materials; 6% applies to modern services; and exports are zero-rated. Small businesses on the simplified regime use a reduced 1% rate in 2026–2027 instead of the usual 3%.

Yes. Exports are zero-rated with the right to recover input VAT. Only general taxpayers registered as exporters can claim, and the amount is set by product-specific refund (rebate) rates that often differ from the standard rate.

From 1 April the rebate was cut or scrapped for several product groups — photovoltaic products such as solar panels lost it entirely. Battery rebates were first reduced, then zeroed from 2027. The trigger is the export date on the customs declaration, not the contract date.

It is charged at customs on the customs value plus duty (plus consumption tax where it applies), multiplied by the relevant rate. The product type decides whether that is 13, 9 or 6 percent.

No. Hong Kong is a separate tax territory with no value-added tax at all, unlike the mainland. It is one of the fundamental differences between the two jurisdictions and matters when planning shipments.